Audit reporting: The 4 types of audit opinions & reports

In audit reporting, an auditor compiles and delivers their opinion about the audit results. As simple as that may sound, audit reports can actually be quite complicated. Some information required for audit reporting isn’t readily available, and some information is subjective. Not to mention, there are multiple types of audit reports and opinions an auditor can deliver.

When done well, an audit report can give the board, its audit committee and investors deep insight into the organization’s financial performance. They also allow auditors to comment on a company’s financial reporting and offer opportunities for improvement. To help companies understand what to expect from their next audit, this article will explain:

- What an audit report is

- What an audit opinion is

- The four types of audit reports and opinions

Obtaining a favorable audit opinion

What is an audit report.

An audit report is a document in which an auditor shares their opinion on an organization’s financial performance and whether they’re compliant with financial reporting regulations. Auditors must follow the format defined by the generally accepted auditing standards (GAAS), with some exceptions depending on the nature of the audit.

That said, audit reports will generally include a description of the auditor’s role, management’s role, the scope of the audit and the audit opinion.

What is the purpose of an audit report?

The purpose of an audit report is to make a statement about a company’s financial status related to its financial reporting. Annual audits demonstrate transparency in corporate financial reporting, a positive step in establishing good relationships between companies, their investors, and the public.

The audit report provides a picture of a company’s financial performance in a given fiscal year and how effectively the company complies with regulations like the Generally Accepted Accounting Principles.

Investors analyze audit reports and base much of their investment decisions on information contained in the audit reports. Regulators will also review audit reports to decide whether to assess penalties for noncompliance.

When do auditors prepare their reports?

Before the audit, management provides financial information to the audit committee. During the annual audit, the auditor has to review the processes and procedures that the company used to prepare the financial information. After the audit, the auditors prepare the audit reports, including checking to see whether the company uses GAAP or other applicable reporting frameworks.

The 5 C’s of audit reporting

Though the contents of an audit report can vary slightly based on the auditor’s opinion, most reports will include the auditor’s point of view on what’s called the 5 C’s of audit report writing. These are:

- Condition: What is the item being reviewed?

- Criteria: What did the organization meet or fail to meet? This could range from a misstatement to a regulatory infraction.

- Cause: What made the issue possible?

- Consequence: What is the outcome of the auditor’s finding?

- Corrective action: How should the organization mitigate the issue?

What are the components of an audit report?

Audit reports typically have seven different components ranging from the auditor’s signature to their recommendations for the audited company. These components are:

- Report title: Most audit report titles should be straightforward and can indicate whether the auditor is independent or not.

- Introduction: This section is typically a short paragraph that includes the company and duration under audit.

- Scope: This section is roughly a paragraph and defines what the auditor reviewed.

- Executive summary: The auditor briefly summarizes the audit results and their opinion.

- Opinion: Following the executive summary, the auditor will provide more detail about their opinion and what it means for the organization.

- Auditor’s name and signature: The auditor will close the report with their name and signature.

What is an audit opinion?

An audit opinion is a section of the audit report explaining the audit results.

The audit opinion is based on several variables. The audit opinion is based on several variables. For example:

- How available the data was to them

- Whether they had an opportunity to follow all due procedures

- The level of materiality

Each of these variables is subjective and depends on the auditor’s opinion.

An adverse audit opinion can damage a company’s status. In some cases, adverse audit opinions may lead to litigation. Regulatory bodies may also scrutinize the audit opinion and the audit report to verify the information for accuracy and any impact on taxation matters.

The 4 types of audit opinions

Auditors can choose among four different types of auditor opinion reports. An auditor opinion report is a letter that auditors attach to the statutory audit report that reflects their opinion of the audit. The four audit opinion types are:

Unqualified opinion – clean report

An unqualified opinion is considered a clean report. This is the type of report that auditors give most often. It is also the type of report that most companies expect to receive.

An unqualified opinion doesn’t have any adverse comments, and it doesn’t include any disclaimers about any clauses or the audit process.

Why an auditor issues an unqualified opinion

This report indicates that the auditors are satisfied with the company’s financial reporting. The auditor believes the company’s operations comply with governance principles and applicable laws. The company, the auditors, the investors and the public perceive such a report to be free from material misstatements.

Unmodified opinion

An unmodified opinion is the same as an unqualified opinion, but the difference comes down to context. Clean audit reports for publicly listed companies have an unqualified opinion, while those same reports for private companies are considered unmodified.

Qualified opinion – qualified report

A qualified opinion results in a qualified report. It typically indicates that the auditor isn’t confident about any specific process or transaction, which prevents them from issuing an unqualified or clean report. Investors don’t find qualified opinions acceptable, as they project a negative opinion about a company’s financial status.

Auditors write up a qualified opinion in much the same way as an unqualified opinion, with the exception that they state the reasons they’re not able to present an unqualified opinion.

Why an auditor issues a qualified opinion

An auditor will give a qualified opinion and qualified report if they can’t confidently clear the organization's financial statements or financial reporting practices. A common reason for auditors issuing a qualified opinion is that the company didn’t present its records with GAAP.

Disclaimer of opinion – disclaimer report

A disclaimer of opinion results in a disclaimer report. When an auditor issues a disclaimer of opinion report, it means that they are distancing themselves from providing any opinion at all related to the financial statements.

The general consensus is that a disclaimer of opinion constitutes a very harsh stance. As a result, it creates an adverse image of the company.

Why an auditor issues a disclaimer of opinion

Some of the reasons that auditors may issue a disclaimer of opinion are because they felt like the company limited their ability to conduct a thorough audit or they couldn’t get satisfactory explanations for their questions. They may not have been able to decipher the correct nature of some transactions or to secure enough evidence to support good financial reporting.

Auditors who aren’t allowed an opportunity to observe operational procedures or to review particular procedures may feel like they’re not able to express a definite opinion, so they feel a disclaimer is necessary and in order.

Adverse opinion – adverse audit report

The final type of audit opinion is an adverse opinion. An auditor’s adverse opinion is a big red flag. An adverse audit report usually indicates that financial reports contain gross misstatements and have the potential for fraud.

Why an auditor issues an adverse opinion

Auditors who aren’t at all satisfied with the financial statements or who discover a high level of material misstatements or irregularities know that this creates a situation in which investors and the government will mistrust the company’s financial reports.

Adverse opinions send out a high alert that the company’s records haven’t been prepared according to GAAP. Financial institutions and investors take this opinion seriously and will reject doing any kind of business with the company.

Auditors form their opinions by making professional judgments and getting legal opinions. To satisfy auditors’ keen eye and earn an unqualified opinion, it’s vital that companies:

- Implement internal controls: Internal controls not only lead to better financial statements, but they also make financial performance more defensible to auditors .

- Create strong financial policies: It’s easier to build a compliant financial reporting process than it is to fix one with deep-seated flaws. Create and implement policies with GAAP in mind.

- Conduct regular reviews: Organizations should have financial controls and policies reviewed regularly by the company’s internal audit team to ensure that everything is in order before the audit ensues.

- Utilize software solutions: Board management software programs support the accountability and transparency of financial reporting to ensure that companies get the best auditor opinion letter, while audit management solutions ensure that companies are well positioned to earn unqualified opinions in their audit reports. It drives efficiency across the audit workflow with built-in best practices and a solution that scales with you.

Modernize your approach to audit reporting

Auditors use all types of qualified reports to alert the public as to the transparency, reliability and accountability of companies. Auditor opinions place pressure on companies to change their financial reporting processes and pay closer attention to practices like ESG so that they’re clear and accurate. Companies, investors and the public highly value unqualified reports.

Efficient management of the audit process, coupled with a modernized approach, allows your organization to stay ahead of emerging risks. From empowering informed decision-making to automated, time-saving processes, Diligent’s Audit Management solution helps you to deliver audit reports with ease.

Solutions Solutions

- Board Management

- Enterprise Risk Management

- Audit Management

- Market Intelligence

Resources Resources

- Research & Reports

Company Company

Your data matters.

4 levels of audit opinions

The first page of audited financial statements is the auditor’s report. This is an important part of the financials that shouldn’t be overlooked. It contains the audit opinion, which indicates whether the financial statements are fairly presented in all material respects, compliant with Generally Accepted Accounting Principles (GAAP) and free from material misstatement.

In general, there are four types of audit opinions, ranked from most to least desirable.

1. Unqualified

A clean “unqualified” opinion is the most common (and desirable). Here, the auditor states that the company’s financial condition, position and operations are fairly presented in the financial statements.

2. Qualified

The auditor expresses a qualified opinion if the financial statements appear to contain a small deviation from GAAP but are otherwise fairly presented. To illustrate: An auditor will “qualify” his or her opinion if a borrower incorrectly estimates the reserve for a contingency, but the exception doesn’t affect the rest of the financial statements.

Qualified opinions are also given if the company’s management limits the scope of audit procedures. For example, a qualified opinion may have resulted if you denied the auditor access to year-end inventory counts due to safety concerns during the COVID-19 pandemic.

3. Adverse

When an auditor issues an adverse opinion, there are material exceptions to GAAP that affect the financial statements as a whole. Here, the auditor indicates that the financial statements aren’t presented fairly. Typically, an adverse opinion letter outlines these exceptions.

4. Disclaimer

Even more alarming to lenders and investors is a disclaimer opinion. Disclaimers occur when an auditor gives up in the middle of an audit. Reasons for disclaimers may include significant scope limitations, material doubt about the company’s going-concern status and uncertainties within the subject company itself. A disclaimer opinion letter briefly outlines the auditor’s reasons for throwing in the towel.

Beyond the opinion

Auditors’ reports for public companies also must include a discussion of so-called “critical audit matters” (CAMs). Essentially, these are the most complicated issues that arose during the audit. CAMs are specific to the engagement and the year of the audit. As a result, they’re expected to change from year to year.

This requirement represents a major change to the pass-fail audit opinions that have been in place for decades. It’s intended to give stakeholders greater insight into the company’s disclosures and the auditor’s work when issuing an unqualified opinion. Contact us for more information on audit opinions.

Other Reads:

1100 Sunset Lane Suite 1310 P.O. Box 1507

Culpeper, VA 22701

3110 Fairview Park Dr, Suite 1100, Falls Church, VA 22042

1320 Central Park Blvd., Suite 405 Fredericksburg, VA 22401

608 South King Street Suite 200 P.O. Box 3307 Leesburg, VA 20177

4423 Pheasant Ridge Road, Suite 115 Roanoke, VA 24014

50 South Cameron Street, Winchester, VA, United States

6 South Pendleton Street, Middleburg, VA, United States

10451 Mill Run Circle, Suite 800, Owings Mills, MD 21117

9954 Mayland Drive, Richmond, VA, United States

702 King Farm Blvd., Suite 610 Rockville, MD 20850

- Wealth Insights

- Blog & Press Releases

- Inclusion & Diversity

- SafeSend Returns

- SafeSend Organizers

- Financial Statement Audit

- Review, Compilation & AUP

- Retirement Plan Audits

- Employee Retention Credit Consulting

- Personal & Business Tax Services

- Tax Services for Banks

- Not-for-Profit Tax Preparation

- CAAS | Outsourced CFO

- QuickBooks ProAdvisor

- Wealth Management

- Estate & Trust Planning

- Family Office

- Litigation Support

- Risk Advisory

- Agribusiness & Manufacturing

- Architecture, Engineering, & Construction

- Community Banks

- Credit Unions

- Government Contracting

- Hospitality

- Physician Practices

- Health Care Organizations

- Private Client Services

- Professional Service Firms

- Not-for-Profit

- Experienced

- College & Entry Level

- Past Webinars

- Submit Request for Proposal

- Sign Up for Our Newsletter

- Client Portal

- Skip to main content

- Skip to "About this site"

- Skip to section menu

Language selection

- Search and menus

COPYRIGHT NOTICE — This document is intended for internal use. It cannot be distributed to or reproduced by third parties without prior written permission from the Copyright Coordinator for the Office of the Auditor General of Canada. This includes email, fax, mail and hand delivery, or use of any other method of distribution or reproduction. CPA Canada Handbook sections and excerpts are reproduced herein for your non-commercial use with the permission of The Chartered Professional Accountants of Canada (“CPA Canada”). These may not be modified, copied or distributed in any form as this would infringe CPA Canada’s copyright. Reproduced, with permission, from the CPA Canada Handbook, The Chartered Professional Accountants of Canada, Toronto, Canada.

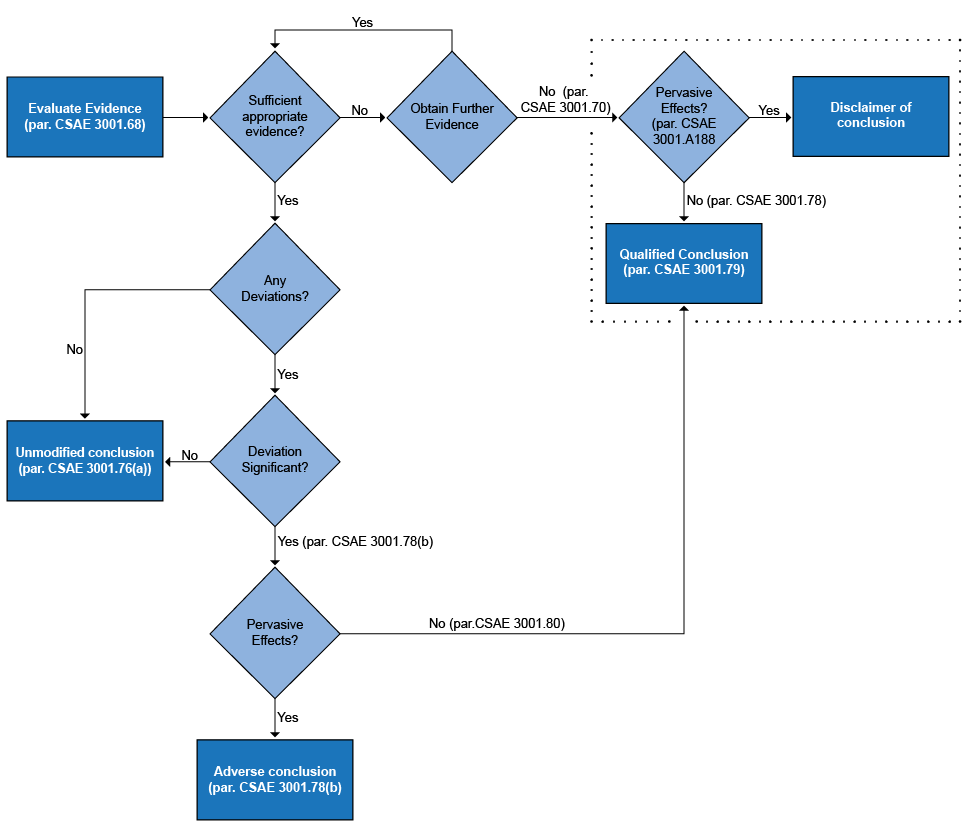

7040 Audit Conclusion Jul-2020 Last Reviewed : 03-Oct-2017 -->

This section presents the requirements pertaining to the audit conclusion. It provides guidance on the four types of conclusion that are possible to reach as well as guidance on what to consider when forming a conclusion. There is also a specific reference to how to form a special examination opinion, including the concept of significant deficiency.

CSAE 3001 Requirements

21. If an objective in this CSAE or a relevant subject-matter-specific CSAE cannot be achieved, the practitioner shall evaluate whether this requires the practitioner to modify the practitioner’s conclusion or withdraw from the engagement (where withdrawal is possible under applicable law or regulation). Failure to achieve an objective in a relevant CSAE represents a significant matter requiring documentation in accordance with paragraph 82 of this CSAE.

28. If the engaging party imposes a limitation on the scope of the practitioner’s work in the terms of a proposed direct engagement such that the practitioner believes the limitation will result in the practitioner disclaiming a conclusion on the underlying subject matter, the practitioner shall not accept such an engagement as an assurance engagement, unless required by law or regulation to do so. (Ref: Para. A156(c))

34. In some cases, law or regulation of the relevant jurisdiction prescribe the layout or wording of the assurance report. In these circumstances, the practitioner shall evaluate:

(a) Whether intended users might misunderstand the assurance conclusion; and

(b) If so, whether additional explanation in the assurance report can mitigate possible misunderstanding.

If the practitioner concludes that additional explanation in the assurance report cannot mitigate possible misunderstanding, the practitioner shall not accept the engagement, unless required by law or regulation to do so. An engagement conducted in accordance with such law or regulation does not comply with CSAEs. Accordingly, the practitioner shall not include any reference within the assurance report to the engagement having been conducted in accordance with this CSAE or any other CSAE(s) (see also paragraph 75).

48. If it is discovered after the engagement has been accepted that some or all of the underlying subject matter is not appropriate for an assurance engagement, the practitioner shall consider withdrawing from the engagement, if withdrawal is possible under applicable law or regulation. If the practitioner continues with the engagement, the practitioner shall express a qualified conclusion or disclaimer of conclusion, as appropriate in the circumstances. (Ref: Para. A89)

49. The practitioner shall consider significance when: (Ref: Para. A90-A98)

(b) Evaluating whether the underlying subject matter is free from significant deviation.

56. The practitioner shall consider whether individual deviations identified during the engagement (other than those that are clearly trivial) have characteristics, for example a root cause or a problematic pattern, that indicate the aggregate effect of individual deviations is likely to be significant. (Ref: Para A120)

65. If one or more of the requested written representations are not provided or the practitioner concludes that there is sufficient doubt about the competence, integrity, ethical values, or diligence of those providing the written representations, or that the written representations are otherwise not reliable, the practitioner shall: (Ref: Para. A140)

(a) Discuss the matter with the appropriate party(ies);

(b) Reevaluate the integrity of those from whom the representations were requested or received and evaluate the effect that this may have on the reliability of representations (oral or written) and evidence in general; and

(c) Take appropriate actions, including determining the possible effect on the conclusion in the assurance report.

68. The practitioner shall evaluate the sufficiency and appropriateness of the evidence obtained in the context of the engagement and, if necessary in the circumstances, attempt to obtain further evidence. The practitioner shall consider all relevant evidence, regardless of whether it appears to corroborate or to contradict the measurement or evaluation of the underlying subject matter against the applicable criteria. If the practitioner is unable to obtain necessary further evidence, the practitioner shall consider the implications for the practitioner’s conclusion in paragraph 69. (Ref: Para. A147-A153)

69. The practitioner shall form a conclusion about whether the underlying subject matter is free from significant deviation. In forming that conclusion, the practitioner shall consider the practitioner’s conclusion in paragraph 68 regarding the sufficiency and appropriateness of evidence obtained and an evaluation of whether identified deviations are significant, individually or in the aggregate. (Ref: Para. A5, A120 and A154-A155)

70. If the practitioner is unable to obtain sufficient appropriate evidence, a scope limitation exists and the practitioner shall express a qualified conclusion, disclaim a conclusion, or withdraw from the engagement, where withdrawal is possible under applicable law or regulation, as appropriate. (Ref: Para. A156-A158)

71. The assurance report shall be in writing and shall contain a clear expression of the practitioner’s conclusion about the underlying subject matter. (Ref: Para. A4, A159-A161)

72. The practitioner’s conclusion shall be clearly separated from information or explanations that are not intended to affect the practitioner’s conclusion, including any findings related to particular aspects of the engagements, recommendations or additional information included in the assurance report. The wording used shall make it clear that findings, recommendations or additional information is not intended to detract from the practitioner’s conclusion. (Ref: Para. A159-A161)

73. The assurance report shall include at a minimum the following basic elements:

(l) The practitioner's conclusion on the objective of the engagement: (Ref: Para. A2-A4, A176-A181)

(i) When appropriate, the conclusion shall inform the intended users of the context in which the practitioner's conclusion is to be read. (Ref: Para. A178)

(ii) In a reasonable assurance engagement, the conclusion shall be expressed in a positive form. (Ref: Para. A177)

(iv) The conclusion in (ii) or (iii) shall be phrased using appropriate words for the underlying subject matter and applicable criteria given the engagement circumstances.

(v) When the practitioner expresses a modified conclusion, the report shall contain:

a. A section that provides a description of the matter(s) giving rise to the modification; and

b. A section that contains the practitioner's modified conclusion. (Ref: Para. A181)

75. If the practitioner is required by law or regulation to use a specific layout or wording of the assurance report, the assurance report shall refer to this or other CSAEs only if the assurance report includes, at a minimum, each of the elements identified in paragraph 73.

76. The practitioner shall express an unmodified conclusion when the practitioner concludes:

(a) In the case of a reasonable assurance engagement, that the underlying subject matter complies, in all significant respects, with the applicable criteria; or

77. If the practitioner considers it necessary to communicate a matter other than those specifically related to the underlying the subject matter that, in the practitioner’s judgment, is relevant to intended users’ understanding of the engagement, the practitioner’s responsibilities or the assurance report, and this is not prohibited by law or regulation, the practitioner shall do so in a paragraph in the assurance report, with an appropriate heading, that clearly indicates the practitioner’s conclusion is not modified in respect of the matter.

78. The practitioner shall express a modified conclusion in the following circumstances:

(a) When, in the practitioner’s professional judgment, a scope limitation exists and the effect of the matter could be significant (see paragraph 70). In such cases, the practitioner shall express a qualified conclusion or a disclaimer of conclusion.

(b) When, in the practitioner’s professional judgment, there is a significant deviation in the underlying subject matter. In such cases, the practitioner shall express a qualified conclusion or adverse conclusion. (Ref: Para. A190)

79. The practitioner shall express a qualified conclusion when, in the practitioner’s professional judgment, the effects, or possible effects, of a matter are not so significant and pervasive as to require an adverse conclusion or a disclaimer of conclusion. A qualified conclusion shall be phrased to inform the intended users of the effects, or possible effects, of the matter to which the qualification relates. (Ref: Para. A187-A190)

80. If the practitioner expresses a modified conclusion because of a scope limitation but is also aware of a matter(s) that causes a significant deviation in the underlying subject matter, the practitioner shall include in the assurance report a clear description of both the scope limitation and the matter(s) that causes the significant deviation.

CSAE 3001 Application Material

A2. The practitioner in a performance audit describes in the report the objective of the engagement and the underlying subject matter so that the reader can understand and properly interpret the results. The wording of the objective would be determined by the circumstances of the engagement. For example, the objective for a performance audit may be to conclude whether the entity being audited has adequately managed a program so that the entity’s key responsibilities under that program have been met. The practitioner’s conclusion relates to the objective and scope of the engagement and follows logically from the description of the criteria and findings. If the engagement has more than one objective, the assurance report provides a conclusion on each objective.

A4. Where the underlying subject matter is made up of a number of aspects, separate conclusions may be provided on each aspect. All such separate conclusions do not need to relate to the same level of assurance. Rather, each conclusion is expressed in the form that is appropriate to either a reasonable assurance engagement or a limited assurance engagement. References in this CSAE to the conclusion in the assurance report include each conclusion when separate conclusions are provided.

A98. Concluding on the significance of the deviations identified as a result of the procedures performed requires professional judgment. For example:

- The applicable criteria for a performance audit for a hospital’s emergency department may include the speed of the services provided, the quality of the services, the number of patients treated during a shift, and benchmarking the cost of the services against other similar hospitals. If three of these applicable criteria are satisfied but one applicable criterion is not satisfied by a small margin, then professional judgment is needed to conclude whether the hospital’s emergency department represents value for money as a whole.

- In a compliance engagement, the entity may have complied with nine provisions of the relevant law or regulation, but did not comply with one provision. Professional judgment is needed to conclude whether the entity complied with the relevant law or regulation as a whole. For example, the practitioner may consider the importance of the provision with which the entity did not comply, as well as the relationship of that provision to the remaining provisions of the relevant law or regulation.

A120. “Clearly trivial” is not another expression for “not significant.” Matters that are clearly trivial will be of a wholly different (smaller) order of importance than significance determined in accordance with paragraph 49, and will be matters that are clearly inconsequential, whether taken individually or in aggregate and whether judged by any criteria of size, nature or circumstances. When there is any uncertainty about whether one or more items are clearly trivial, the matter is considered not to be clearly trivial.

A152. Whether sufficient appropriate evidence has been obtained on which to base the practitioner’s conclusion is a matter of professional judgment.

A155. The practitioner’s professional judgment as to what constitutes sufficient appropriate evidence is influenced by such factors as the following:

- Importance of a potential deviation and the likelihood of its having a significant effect, individually or when aggregated with other potential deviations, on the practitioner’s report.

- Effectiveness of the appropriate party(ies)’s responses to address the known risk of significant deviation.

- Experience gained during previous assurance engagements with respect to similar potential deviations.

- Results of procedures performed, including whether such procedures identified specific deviations.

- Source and reliability of the available information.

- Persuasiveness of the evidence.

- Understanding of the appropriate party(ies) and its environment.

A156. A scope limitation may arise from:

(a) Circumstances beyond the control of the appropriate party(ies). For example, documentation the practitioner considers to be necessary to inspect may have been accidentally destroyed;

(b) Circumstances relating to the nature or timing of the practitioner’s work. For example, a physical process the practitioner considers to be necessary to observe may have occurred before the practitioner’s engagement; or

(c) Limitations imposed by the responsible party or the engaging party on the practitioner that, for example, may prevent the practitioner from performing a procedure the practitioner considers to be necessary in the circumstances. Limitations of this kind may have other implications for the engagement, such as for the practitioner’s consideration of engagement risk and engagement acceptance and continuance.

A157. An inability to perform a specific procedure does not constitute a scope limitation if the practitioner is able to obtain sufficient appropriate evidence by performing alternative procedures.

A177. An example of a conclusion expressed in a form appropriate for a reasonable assurance engagement is: “In our opinion, the entity has complied, in all significant respects, with XYZ law.”

A178. It may be appropriate to inform the intended users of the context in which the practitioner’s conclusion is to be read when the assurance report includes an explanation of particular characteristics of the underlying subject matter of which the intended users should be aware. The practitioner’s conclusion may, for example, include wording such as: “This conclusion has been formed on the basis of the matters outlined elsewhere in this independent assurance report.”

A180. Forms of expression which may be useful for underlying subject matters include, for example, “in compliance with” or “in accordance with.”

A181. Inclusion of a heading above paragraphs containing modified conclusions, and the matter(s) giving rise to the modification, aids the understandability of the practitioner’s report. Examples of appropriate heading include “Qualified Conclusion,” “Adverse Conclusion,” or “Disclaimer of Conclusion” and “Basis for Qualified Conclusion,” “Basis for Adverse Conclusion,” as appropriate.

A187. The words “except for” are commonly used to indicate the matter(s) to which a qualification relates. However, other wording may be used to clearly indicate those matter(s).

A188. The term “pervasive” describes the effects on the underlying subject matter of deviations or the possible effects on the underlying subject matter of deviations, if any, that are undetected due to an inability to obtain sufficient appropriate evidence. Pervasive effects on the underlying subject matter are those that, in the practitioner’s professional judgment:

(a) Are not confined to specific aspects of the underlying subject matter; or

(b) If so confined, represent or could represent a substantial proportion of the underlying subject matter.

A189. The nature of the matter, and the practitioner’s judgment about the pervasiveness of the effects or possible effects on the underlying subject matter, affects the type of conclusion to be expressed.

A190. Examples of qualified and adverse conclusions and a disclaimer of conclusion are:

- Qualified conclusion (an example for limited assurance engagements with a significant deviation) – “Based on the procedures performed and the evidence obtained, except for the effect of the matter described in the Basis for Qualified Conclusion section of our report, nothing has come to our attention that causes us to believe that the entity has not complied, in all significant respects, with XYZ law.”

- Qualified conclusion (an example for reasonable assurance engagements with a significant deviation) – “We conclude that the entity increased the capacity of its facilities in a manner that meets its needs in the short term. However, the entity did not develop a long-term plan to ensure its capacity needs will be met in the future.”

- Adverse conclusion (an example for a significant and pervasive deviation for both reasonable assurance and limited assurance engagements) – “Because of the importance of the matter described in the Basis for Adverse Conclusion section of our report, the entity has not complied, in all significant respects, with XYZ law.”

- Disclaimer of conclusion (an example for a significant and pervasive limitation of scope for both reasonable assurance and limited assurance engagements) – “Because of the importance of the matter described in the Basis for Disclaimer of Conclusion section of our report, we have not been able to obtain sufficient appropriate evidence to form a conclusion on the on whether the entity has complied, in all significant respects, with XYZ law. Accordingly, we do not express a conclusion on such compliance.”

Financial Administration Act Requirements for Special Examinations

Section 139(1) An examiner shall, on completion of the special examination, submit a report on his findings to the board of directors of the corporation examined.

(2) The report of an examiner under subsection (1) shall include

(a) a statement whether in the examiner’s opinion, with respect to the criteria established pursuant to subsection 138(3), there is reasonable assurance that there are no significant deficiencies in the systems and practices examined; and

(b) a statement of the extent to which the examiner relied on internal audits.

Audits shall have a clear conclusion against the audit objective. [Nov-2016]

OAG Guidance

What the csae 3001 means for the audit conclusion.

The standard requires that the audit concludes against the audit objective and that the conclusion is clearly indicated in the audit report.

The standard also requires that the engagement leader supports the audit conclusion with sufficient appropriate evidence, and that he/she forms a conclusion about whether the subject matter is free from significant deviation (see OAG Audit 2020 Significance).

If the evidence shows that one or more of the audit criteria have not been met, then the engagement leader must use professional judgment to decide whether to express a “reservation” in the form of a qualified or an adverse conclusion, and explain the reason for the reservation in the audit report.

If the team has been unable to obtain sufficient appropriate evidence regarding an entity’s conformity with any of the audit criteria, we have a scope limitation. The standards require that the engagement leader expresses a qualified conclusion, disclaims a conclusion, or withdraws from the audit. A disclaimer of conclusion rarely occurs in the OAG’s performance audits and could not occur in special examinations.

The following diagram illustrate the steps set out in CSAE 3001 in forming the conclusion, with relevant paragraph numbers referenced.

How to form a conclusion

In forming conclusions, using their professional judgment, the auditors evaluate the sufficiency and appropriateness of the evidence obtained (see OAG Audit 7021 Evaluate sufficiency and appropriateness of audit evidence, and OAG Audit 1051 Sufficient appropriate audit evidence). They also assess the significance (see OAG Audit 2020 Significance) of the findings in relation to the audit objective. The conclusion should not be a summary of findings, but rather be a clear conclusion against the audit objective.

The conclusion has to be expressed using a positive form; for example, “The entity has complied, in all significant respects, with xyz . . .”

There are essentially four different types of conclusions that can be used in direct engagements:

- unmodified (clean) conclusion (“yes”);

- qualified conclusion (“yes, but” or “no, but”);

- adverse conclusion (“no”); and

- disclaimer of conclusion (when the audit team is unable to conclude due to lack of sufficient appropriate evidence).

Audit team members need to clearly communicate the type of conclusion in the audit report. They also need to use professional judgment in forming a conclusion ( OAG Audit 1042 Applying professional judgment). For example, the team may decide to qualify the conclusion when some parts of an entity’s performance are satisfactory while others are unsatisfactory. The conclusion can then contain an "except for" statement to disclose the deviations from satisfactory performance.

If it is an unmodified (clean) conclusion (“yes”) or an adverse conclusion (“no”), the audit team should echo the words of the audit objective(s) in the conclusion. In an adverse conclusion, the audit team should also ensure to have a very clear “no.” An adverse conclusion is used when the significance and extent of the deviations from satisfactory performance are pervasive. When performance is fully satisfactory or highly unsatisfactory, concluding against the overall objective may be straightforward and the audit report will reflect a completely positive or adverse conclusion, as appropriate.

A qualified conclusion (“yes, but” / “no, but”) should contain the following essential elements: (1) clear announcement of the conclusion with specific reference to the audit objective, (2) clear “placement” (“yes, but / no, but”), and (3) reason for the (“yes, but / no, but”). For example:

(1) We conclude that the Department of Widget Affairs administered its Widget program in accordance with the Widgets Act, (2) with some improvement required in communications. (3) In particular , Widget status reports need to be communicated from headquarters to regional offices sooner so that Widget officers in the field have up-to-date lists of fees to be charged.

The core of a clear overall audit report conclusion is a single key paragraph with a clear overall conclusion. In straightforward cases, the entire conclusion may only be one paragraph. In more complex cases (multiple auditees, not a clean conclusion, etc.), further explanatory paragraphs can be added if the conclusion is not self-evident. The conclusion should be in a separate section of the written audit report in order to make it clear to the readers that this is the conclusion of the audit, not a finding on a specific aspect of the audit or a recommendation (see OAG Audit 7030 Drafting the audit report).

If, despite best efforts, an audit team is unable to obtain sufficient appropriate evidence, it may report the available evidence and its limitations, but it cannot draw findings and conclusions from the evidence. If the OAG decides to report the matter, it would state it as a qualification to the conclusion—that the auditors could not evaluate part of the subject matter because of lack of evidence (i.e. scope limitation). When the lack of evidence is significant, the audit report will express a “disclaimer of conclusion” due to incapacity to obtain sufficient appropriate audit evidence.

If the audit team determines there is a scope limitation (which occurs when the team is unable to obtain sufficient appropriate evidence), it would either explain it in the conclusion using a qualified conclusion or a disclaimer of conclusion (as explained above).

Special examinations

Special examination opinion statement and conclusion. Consistent with sub-paragraph 139(2)(a) of the Financial Administration Act (FAA), each special examination report must include a statement on whether in the examiner’s opinion and based on the established criteria, reasonable assurance exists that there are no significant deficiencies in the Crown corporation’s systems and practices examined.

The special examination opinion statement serves as a basis for the conclusion against the audit objective and is included in the conclusion paragraph in the audit report.

The special examination conclusion can take one of the following forms:

Unmodified (clean) conclusion. In our opinion, based on the criteria established, there was reasonable assurance there were no significant deficiencies in the Corporation’s systems and practices that we examined. We concluded that the Corporation maintained its systems and practices during the period covered by the audit in a manner that provided the reasonable assurance required under section 138 of the Financial Administration Act.

Qualified conclusion (one significant deficiency). In our opinion, based on the criteria established, there was a significant deficiency in the Corporation’s [identify specific systems and practices named in report], but there was reasonable assurance there were no significant deficiencies in the other systems and practices that we examined. We concluded that, except for this significant deficiency, the Corporation maintained its systems and practices during the period covered by the audit in a manner that provided the reasonable assurance required under section 138 of the Financial Administration Act.

Qualified conclusion (two significant deficiencies). In our opinion, based on the criteria established, there were significant deficiencies in the Corporation’s [identify the two systems and practices named in report], but there was reasonable assurance there were no significant deficiencies in the other systems and practices that we examined. We concluded that, except for these significant deficiencies, the Corporation maintained its systems and practices during the period covered by the audit in a manner that provided the reasonable assurance required under section 138 of the Financial Administration Act.

Adverse conclusion. In our opinion, based on the criteria established, there were significant deficiencies in the Corporation’s systems and practices that we examined for corporate management and management of operations. As a result of the pervasiveness of these significant deficiencies, we concluded that the Corporation had not maintained its systems and practices during the period covered by the audit in a manner that provided the reasonable assurance required under section 138 of the Financial Administration Act.

Because the FAA prescribes the need to provide a statement of opinion on the systems and practices selected for examination, a disclaimer of conclusion is not an option for special examinations . In the special examination practice, the ability to report on a significant deficiency replaces the need to disclaim a conclusion. If, for example, there was an inability to obtain sufficient appropriate evidence related to one of the areas selected for examination, the engagement team would either opine that there is a significant deficiency in the specific area (i.e. it would issue a qualified conclusion) or, where the inability affects multiple areas, that there is no reasonable assurance that the corporation’s systems and practices selected for examination achieved the statutory control objectives (i.e. the team would issue an adverse conclusion).

The special examination report template prescribes where the opinion should be located in the audit report as well as the exact wording of the statement/conclusion to be used in the possible scenarios (unmodified, qualified, or adverse) (see OAG Audit 7030 Drafting the audit report).

What is a significant deficiency? The FAA prescribes the use of the words “significant deficiency” to be used in the opinion, but does not define what it is. The OAG considers a significant deficiency to have occurred when there is a significant deviation from criteria. A significant deficiency is reported when the systems and practices examined did not meet the criteria established, resulting in a finding that the Corporation could be prevented from having reasonable assurance that its assets are safeguarded and controlled, its resources are managed economically and efficiently, and its operations are carried out effectively.

Significance is judged in relation to the reasonable prospect of a matter influencing the judgments or decisions of a user of a special examination report. For example, factors that may influence the engagement team’s judgment on what is significant in a particular circumstance might include the potential public, legislative, economic, or environmental impact.

Clearly, the definition of “significant” is a matter of judgment and depends on the circumstances. Ultimately, one of the major deciding factors is the identified or potential impact of a deficiency.

Factors considered to determine if a significant deficiency exists. The engagement team may take the following factors into account when determining whether a finding constitutes a significant deficiency:

Extent of deviation from criteria. A finding should be clearly linked to criteria and, for it to be significant, there should be substantial deviation from criteria. Where there are deviations, the engagement team needs to establish whether there are compensating systems or practices to help achieve the desired result.

Impact of the deficiency. To be significant, the deficiency’s impact on achieving the corporation’s statutory control objectives should be clear, serious, and consequential. When selecting key systems and practices and developing criteria, considering the corporation’s exposure to risk will help trace the impact of any deficiencies subsequently identified. The impact may be potential; that is, the consequences may not have materialized yet.

Relevance to the board, the Minister, Parliament, or other users of the report. The engagement team should consider what is of interest and relevance to report users. If a finding is of little or no consequence to users, it may not be significant. What is relevant to report users are a finding’s impact (what it will mean to them) and cause (why it happened). Of course, there may be a difference of opinion between what the engagement team believes is relevant to users and the corporation’s views on the issue, in which case the examiner would report the deficiency as significant if convinced of its consequence to users.

Practicality of the solution. If the likely cost of correcting the deficiency is greater than the benefit to be derived, the deficiency’s significance may be questionable.

Number of reported deficiencies. Minor deviations from several criteria may signal minor problems, or may be symptoms of a problem (or theme) of greater significance that should be reported as a significant deficiency.

- Planned corrective actions. If the corporation has action plans in place or even in process to correct deficiencies that have been classified as significant, these deficiencies should still be included in the report as significant because they existed during the examination period and because there is no assurance that the planned actions will correct the problem or that the actions will continue after the report date.

How is a significant deficiency formulated? A significant deficiency must have a clear evidentiary link to a criterion. Problems often occur when the wording used to describe the deficiency is too general; for example, if the significant deficiency does not discuss the impact(s).

In order to be clear and meaningful, a significant deficiency should identify the problem, its cause, and its effect.

All reasoning behind the decision on the significance of a given deficiency must be documented in the examination file.

Related Sections

OAG Audit 1042 Applying professional judgment OAG Audit 1051 Sufficient appropriate audit evidence OAG Audit 2020 Significance OAG Audit 4041 Audit objective OAG Audit 7021 Evaluate sufficiency and appropriateness of audit evidence OAG Audit 7030 Drafting the audit report

Accountinguide

Simple and Easy

Qualified Opinion

Additionally, the qualified opinion is also given when auditors could not obtain sufficient appropriate audit evidence about certain matters and their effect is material but not pervasive . This happens when there is a scope limitation in an audit.

Likewise, auditors usually give a qualified opinion by expressing that the financial statements are free from material misstatements, except for specific transactions or balances, or circumstance .

In this case, the auditors indicate that while there are material misstatements or material scope limitations, they are confined to a specific element of the financial statements which could be isolated; the rest of financial statements are reliable.

Auditors use the phrase “except for” to describe the issues that give rise to the qualification of the opinion in the audit report. Likewise, a qualified opinion in the audit report usually states that “except for…, the financial statements present fairly (or give a true and fair view)….”.

Qualified Opinion Example

For example, a qualified opinion that auditors give on the financial statements of ABC Limited would look like below:

Basis for Qualified Opinion

In the qualified audit opinion report, a basis for qualified opinion paragraph is required as a separate paragraph to explain the circumstances that lead to auditors modifying the opinion in the audit report.

In this case, the basis for qualified opinion paragraph would explain what misstatements are and how they affect the individual line items in financial statements. It would also describe how the balance sheet and income statement would be different if the financial statements are prepared in accordance with applicable accounting standards.

Qualified opinion given by auditors in the audit report can be the result of any of the two conditions as follow:

- On basis that the financial statements contain the material, but not pervasive, misstatement

- On basis that auditors could not gather sufficient and appropriate evidence and the effects are deemed to be material, but not pervasive, on the financial statements.

The words “material but not pervasive on financial statements” mean that the maters, either material misstatements or lack of evidence with material effects on financial statements, can be isolated. In this case, even though they are material, their effects are only on certain transactions or balances; they do not affect the financial statements as a whole. As a result, auditors express only a qualified opinion with the word “except for” (i.e. except for that, everything is good).

On the other hand, if the matters are both material and pervasive, auditors may either express adverse opinion stating that the financial statements do not present fairly (or do not give a true and fair view), or they do not express their opinion on the financial statements at all, which is referred as disclaimer of opinion .

Qualified opinion vs adverse opinion

Unlike qualified opinion, an adverse opinion is an audit opinion that auditors give when financial statements contain misstatement that is both material and pervasive.

While a qualified opinion means that except for specific transactions or balances, everything is okay, an adverse opinion means that financial statements do not present fairly at all.

Another difference to note is that while a qualified opinion could be either due to the material misstatement found or material scope limitation, auditors can only express an adverse opinion when they have obtained sufficient appropriate evidence to support their opinion.

In case that auditors could not obtain sufficient appropriate evidence due to scope limitation and their effect is deemed to be both material and pervasive, auditors need to disclaimer the opinion instead.

However, there is also a similarity between qualified opinion and adverse opinion in addition to the materiality matter. The similarity, in this case, is that both qualified opinion and adverse opinion need a separate paragraph for the basis for modification opinion in the audit report which is “basis for qualified opinion” and “basis for adverse opinion” respectively.

Below table is the summary of the comparison between qualified opinion and adverse opinion:

Reasons for qualified audit opinion

Auditors can express a qualified opinion due to any of the three reasons below:

- Material misstatement

- Scope limitation

- Inadequate disclosure

Qualified opinion due to material misstatement

Qualified opinion due to material misstatement is the case where auditors obtained sufficient appropriate audit evidence to prove that there is a material misstatement in financial statements but such misstatement is not pervasive in nature.

For example, the client’s inventories were not at the lower of cost and net realizable value, and the client’s management was not willing to write down the value of inventories to net realizable value. In this case, auditors need to qualify this matter in the audit report.

Qualified opinion due to scope limitation

Qualified opinion due to scope limitation is the case where auditors could not obtain evidence on certain transactions or balances. However, the effect of such transactions or balances is material but not pervasive.

Some examples of scope limitation include:

- loss of supporting documents

- loss of accounting records

- the client does not allow auditors to send confirmation to its customers or suppliers

- the client does not allow auditors to observe the counting of the physical inventories

- auditors are hired too late to observe the counting of the physical inventories, etc.

Qualified opinion due to inadequate disclosure

Qualified opinion due to inadequate disclosure is the case where the client has not fully disclosed certain matters, that auditors believe to be significant for users, in financial statements. Had the client fully disclosed such matters, auditors may give an unqualified opinion in the audit report instead.

The inadequate disclosure that leads to qualified opinion is usually due to the client does not include all necessary disclosures or the disclosures are not in accordance with applicable accounting standards.

Qualified opinion with going concern

Going concern is usually defined as the company’s ability to continue its operations for the foreseeable future. In general, the foreseeable future here means at least 12 months after the reporting date.

The client usually prepares the financial statements based on the going concern basis of accounting. In other words, the client prepares financial statements based on the assumption that it will continue to operate at least 12 months after reporting date.

Likewise, the client’s managements have responsibilities to assess the company’s ability to operate as going concern and make adequate disclosure in financial statements.

Hence, in an audit, auditors have responsibilities to evaluate whether the management’s use of the going concern basis of accounting is appropriate and whether there is any substantial doubt about the client’s ability to continue its operation to foreseeable future.

So, a qualified opinion with going concern here is the case where auditors express a qualified opinion due to the client’s disclosure or assessment about its going concern status.

Likewise, qualified opinion due to going concern usually happens in two circumstances:

- Inadequate disclosure : this is the case where the client’s use of going concern assumption is appropriate, but a material uncertainty exists. However, the client has not fully disclosed such uncertainty in financial statements.

- Inability to obtain sufficient appropriate evidence: This is the case where the client is unwilling to make or extend its assessment on the going concern to at least 12 months after the reporting date. Hence, auditors will not be able to evaluate management’s assessment of the company’s ability to continue as a going concern (as there is no assessment of 12 months or more to begin with).

Of course, in case that the client’s use of going concern assumption is inappropriate, auditors will have to give an adverse opinion instead if the client did not change its basis of preparation of financial statements (e.g. to liquidation or break-up basis).

Related posts:

- Adverse Opinion

- Unqualified Opinion

- Disclaimer of Opinion

- 4 Types of Audit Report

- Audit Adjustment

The Difference Between a Qualified & Unqualified Audit Report

- Small Business

- Accounting & Bookkeeping

- Audit Reports

- ')" data-event="social share" data-info="Pinterest" aria-label="Share on Pinterest">

- ')" data-event="social share" data-info="Reddit" aria-label="Share on Reddit">

- ')" data-event="social share" data-info="Flipboard" aria-label="Share on Flipboard">

How to Read a Financial Audit Report

What are the 4 types of audit reports, material accounting issues of an audit memo.

- What Is an External Business Audit?

- How to Issue a Corrected Audit Report

In an audit engagement, the auditor gives his opinion on the financial information disclosed by your business. The auditor’s report is an integral element of your business’s audited financial statement. At the culmination of the audit engagement, the auditor expresses his opinion in the auditor’s report, which can be qualified or unqualified.

Audit Report Layout

The auditor’s report begins with a brief introduction about the audit engagement. Thereafter, the auditor’s report is divided in to three major sections. In the first section, the auditor explains that preparing the financial statements and maintaining sound internal controls is management’s responsibility.

In the second section, the auditor explains its own responsibilities, duties and rights regarding the engagement. Here, the auditor emphasizes the nature of the audit and states that the auditor only examines internal controls and accounting records on a sample basis. In the third section, the auditor gives his opinion on the financial statements.

An Unqualified Report

In an unqualified report, the auditors conclude that the financial statements of your business present fairly its affairs in all material aspects. The opinion embodies the assumptions that your business observed compliance with generally accepted accounting principles and statutory requirements. Also known as a clean report, such a report implies that any changes in the accounting policies, their application and effects, are adequately determined and divulged.

This opinion does not tell that your business is in good economic health. It merely states that your financial report is transparent and thorough and has not hidden important facts.

A Qualified Report

A qualified report is one in which the auditor concludes that most matters have been dealt with adequately, except for a few issues. An auditor’s report is qualified when there is either a limitation of scope in the auditor’s work, or when there is a disagreement with management regarding application, acceptability or adequacy of accounting policies. For auditors an issue must be material or financially worth consideration to qualify a report. The issue should not be pervasive, that is, the issue should not misrepresent the factual financial position.

If issues are material and pervasive, the auditor issues a disclaimer or adverse opinion. A qualified audit report does not mean that your business is suffering, and it doesn't mean that your financial statement isn't transparent. It merely reflects the auditor’s inability to give a clean report.

Other Differences in the Opinion Paragraph

Another difference lies in the wording of the opinion paragraph of an auditor’s report. When issuing an unqualified report the auditor might write, “In our opinion, the financial statements give a true and fair view of the financial position of XYZ Enterprises as of ….” Conversely, the opinion paragraph in a qualified report might begin with, “In our opinion, except for the effects of the following adjustments, if any, as might have been determined to be necessary had we been able to perform tests on companies stocks, the financial statements give a true and fair view of the financial position of XYZ Enterprises as …. “

Notice that there are “exceptions” in the opinion paragraph of the qualified report.

Impact of Auditors' Opinions

As a businessperson, you should keep in mind that there are deep-held perceptions about auditors' opinions. Banks, investors and regulators such as the IRS rely on audited financial statements for their analytical needs. Stakeholders such as banks and investors view qualified audit report unfavorably. Therefore, you should hope to receive an unqualified audit report because it gives a positive impression of your business.

For example, if your business was issued a qualified audit report on inventory matters, your bank is more likely to demand further details about your inventory before issuing credit to you.

- PWC: Insights For The Investment Community

- Auditing And Assurance; Vasha Ainapure and Mukind Ainopure

- Auditing and Assurance; Clifford Gomez

- Contemporary Auditing; Kamal Gupta

- PWC: Assurance Today And Tomorrow

Related Articles

What does a report from an auditor look like in a company's annual report, limitation of scope in an audit report, types of audit opinions rendered in accounting, qualified audit report examples, what is a "modified audit opinion", how to prepare an audit report, steps in writing an audit report, types of audit opinion letters, how to build an audit plan, most popular.

- 1 What Does a Report From an Auditor Look Like in a Company's Annual Report?

- 2 Limitation of Scope in an Audit Report

- 3 Types of Audit Opinions Rendered in Accounting

- 4 Qualified Audit Report Examples

The global body for professional accountants

- Search jobs

- Find an accountant

- Technical activities

- Help & support

Can't find your location/region listed? Please visit our global website instead

- Middle East

- Cayman Islands

- Trinidad & Tobago

- Virgin Islands (British)

- United Kingdom

- Czech Republic

- United Arab Emirates

- Saudi Arabia

- State of Palestine

- Syrian Arab Republic

- South Africa

- Africa (other)

- Hong Kong SAR of China

- New Zealand

- Our qualifications

- Getting started

- Your career

- Apply to become an ACCA student

- Why choose to study ACCA?

- ACCA accountancy qualifications

- Getting started with ACCA

- ACCA Learning

- Register your interest in ACCA

- Learn why you should hire ACCA members

- Why train your staff with ACCA?

- Recruit finance staff

- Train and develop finance talent

- Approved Employer programme

- Employer support

- Resources to help your organisation stay one step ahead

- Support for Approved Learning Partners

- Becoming an ACCA Approved Learning Partner

- Tutor support

- Computer-Based Exam (CBE) centres

- Content providers

- Registered Learning Partner

- Exemption accreditation

- University partnerships

- Find tuition

- Virtual classroom support for learning partners

- Find CPD resources

- Your membership

- Member networks

- AB magazine

- Sectors and industries

- Regulation and standards

- Advocacy and mentoring

- Council, elections and AGM

- Tuition and study options

- Study support resources

- Practical experience

- Our ethics modules

- Student Accountant

- Regulation and standards for students

- Your 2024 subscription

- Completing your EPSM

- Completing your PER

- Apply for membership

- Skills webinars

- Finding a great supervisor

- Choosing the right objectives for you

- Regularly recording your PER

- The next phase of your journey

- Your future once qualified

- Mentoring and networks

- Advance e-magazine

- Affiliate video support

- An introduction to professional insights

- Meet the team

- Global economics

- Professional accountants - the future

- Supporting the global profession

- Download the insights app

Can't find your location listed? Please visit our global website instead

- Forming an audit opinion

- Study resources

- Audit and Assurance (AA)

- Technical articles and topic explainers

This article, which is relevant to Paper F8 and P7, revisits the basic principles of forming an audit opinion and looks at how this knowledge should be applied by considering a past Paper P7 exam question

It is one of the most fundamental concepts in auditing; auditors are paid to offer an opinion. It is what they do; it’s their ‘raison d’être.’ Why then, if the audit opinion is so significant, are audit examiners continually underwhelmed by candidates’ appreciation of this topic?

This article, which is relevant to Paper F8 and P7, revisits the basic principles of forming an audit opinion and looks at how this knowledge should be applied by considering a past Pape P7 exam question.

When an auditor is able to satisfactorily conclude that the financial statements are free from material misstatement they express an unmodified opinion. The complete form and content of the unmodified opinion are presented in ISA 700, Forming an Opinion and Reporting on Financial Statements . However, auditors typically use one of two well-known phrases to reflect their conclusion, either:

- ‘The financial statements present fairly, in all material respects...’ or

- ‘The financial statements give a true and fair view of…’

Modifications to the opinion

There are two circumstances when the auditor may choose not to issue an unmodified opinion:

- When the financial statements are not free from material misstatement or

- When they have been unable to obtain sufficient appropriate evidence.

In these circumstances the auditor has to issue a modified version of their opinion. There are three types of modification. Their use depends upon the nature and severity of the matter under consideration.

- the qualified opinion

- the adverse opinion

- the disclaimer of opinion.

Guidance as to the usage of the three forms of modification is provided by ISA 705, Modifications to the Opinion in the Independent Auditor’s Report . This has been summarised in Table 1.

Table 1: Guidance as to the usage of the three forms of audit modification

Pervasiveness is a matter that confuses many candidates as, once again, it is a matter that requires professional judgment. In this case the judgment is whether the matter is isolated to specific components of the financial statements, or whether the matter pervades many elements of the financial statements, rendering them unreliable as a whole.

The bottom line is that if the auditor believes that the financial statements may be relied upon in some part for decision making then the matter is material and not pervasive. If, however, they believe the financial statements should not be relied upon at all for making decisions then the matter is pervasive.

Emphasis of matter

Emphasis of matter (EOM) is rarely dealt with satisfactorily in an exam. This is mainly because candidates believe that EOM is linked somehow to modifications of the opinion. This is not the case: EOM and modified opinions are totally separate matters.

The purpose of an EOM paragraph is to draw the users attention to a matter already disclosed in the financial statements because the auditor believes it is fundamental to their understanding. It is a way of saying to the users: ‘you know that note in the financial statements, the one about the uncertainty surrounding the legal dispute? Well us auditors think it’s really important, so make sure you’ve read it!’

The usage of EOM paragraphs is described in ISA 706, Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report . This identifies three examples of circumstances when the usage of EOM is appropriate:

- when there is uncertainty about exceptional future events

- early adoption of new accounting standards and

- when a major catastrophe has had a major effect on the financial position.

Of course, in all of these examples the auditor can only refer back to disclosures already made in the financial statements. If the directors haven’t disclosed a matter as required by financial reporting standards, then the auditor may conclude that the financial statements are materially misstated and modify the opinion instead.

Other matters

‘Other matter’ paragraphs are used to refer to matters that have not been disclosed in the financial statements that the auditor believes are significant to user understanding. One usage of these paragraphs is where the auditor concludes that there is a material inconsistency between the audited financial statements and the other (unaudited) information contained within the annual report and accounts, as required by ISA 720, The Auditor’s Responsibilities Relating to Other Information in Documents Containing Audited Financial Statements .

Application to exam questions

Now that we have recapped the basic principles of audit opinions let us consider how these may be applied to an exam scenario.

Questions on audit reports in Paper P7 typically fall into two distinct types: critical appraisal of an audit report that has already been written; or explanation of how matters will affect an audit opinion. In both cases the principles affecting the choice of audit opinion are the same.

If you face a question of this nature simplify your task by asking the following questions:

- Is there a misstatement in the financial statements (ie a fraud or error)?

- Has the auditor gathered sufficient appropriate evidence?

- Is/could the matter be material?

- Does the matter pervade the financial statements?

- Does the scenario refer to a disclosure made in the financial statements concerning an uncertain future event?

Based on this approach you should be able to pinpoint exactly what form of opinion is appropriate and whether an EOM paragraph is necessary.

As an example, Question 5 in the June 2009 Paper P7 exam asked candidates to ‘critically appraise the proposed audit report of Pluto Co for the year ended 31 March 2009’. Relevant extracts from the audit report are given in Illustration 1. The full text may be downloaded from the ACCA website.

Please note that the extract is from the International version of the syllabus and refers to International Accounting Standards.

This is largely irrelevant to our understanding of the audit opinion; however, the question does deal with matters where the financial reporting requirements across different accounting regimes are broadly similar. The company in the question is a listed company.

Illustration 1 (when this question was written, ISA 701 was examinable and disagreement with management was a reason for qualifying a report)

Adverse opinion arising from disagreement about application of IAS 37 The directors have not recognised a provision in relation to redundancy costs… and so the recognition criteria of IAS 37 have not been met. We disagree with the directors as we feel that an estimate can be made… We feel that this is a material misstatement as the profit for the year is overstated.

In our opinion, the financial statements do not show a true and fair view of the financial position of the company as of 31 March 2009...

Emphasis of matter paragraph The directors have decided not to disclose the Earnings per share for 2009… Our opinion is not qualified in respect of this matter.

Response – redundancy provision

We are not going to consider the whole wording, merely the choice of opinion. A more complete response is given in the model answer, which can be accessed via the ACCA website.

The first question to ask is whether there is a misstatement. The answer to this is clearly ‘yes’ as the report concludes that the directors have failed to make a provision when they should have. This contravenes the relevant accounting framework (IAS 37, Provisions, Contingent Liabilities and Contingent Assets ). The report also clearly states that this is considered to be material to the financial statements.

Next we have to consider whether the auditor has been able to gather sufficient appropriate evidence. Once again the answer is ‘yes;’ the auditor has been able to reach a considered conclusion on the matter.

At this point we have established that there is a material misstatement. Therefore, we will have to modify our opinion. However, the final version of the modification depends upon whether the matter is pervasive or not.

There is no indication in the audit report that the auditor considers the matter pervasive. It should also be considered that redundancy provisions will only affect two areas of the financial statements: current liabilities and wages/salary costs. Does misstatement here render the remainder of the financial statements unreliable? This is an unlikely conclusion.

It therefore appears unlikely that an adverse opinion is necessary in the circumstances. A qualified (‘except for’) opinion would appear more appropriate.

Earnings per share (EPS) The second issue is that of the EOM paragraph. Ask the question referred to earlier: does the scenario refer to a disclosure made in the financial statements concerning an uncertain future event? Clearly the answer is no. Therefore an EOM paragraph is not appropriate.

If this is the case how should the matter be dealt with? Well, go through the same questions again. First, is there a misstatement?

The directors have failed to disclose the EPS for the year. This contravenes IAS 33, Earnings per Share (and in the UK, FRS 22, Earnings per share ), which requires the basic and diluted EPS to be disclosed in the financial statements of all listed companies. There is, therefore, a misstatement in the financial statements.

Next we consider whether the matter is material. The clarified ISA 320, Materiality in Planning and Performing an Audit requires the auditor to consider the informational requirements of the users. EPS is a vital investor analysis tool and can therefore be considered material by nature. For listed companies, it is a requirement of financial reporting standards that EPS is disclosed with prominence in the financial statements. There is therefore a material misstatement in the financial statements.

Finally the auditor should consider whether the matter is pervasive to the financial statements. The lack of disclosure of the EPS ratio is unlikely to render other elements of the financial statements unreliable; it is an isolated error.

In this instance a qualified opinion should be given on the basis of a material misstatement of the financial statements.

Application to the Paper F8 exam

The concepts considered above are equally as relevant to the Paper F8 exam. However, the wording of the questions to date has been slightly different from the Paper P7 exam. So far candidates have been provided with short scenarios and asked to either state or explain the effects of the matters on the audit report. The approach discussed above may be applied in the same way to these questions.

The matters considered so far (in the December 2007 and December 2009 exams) include: a failure to depreciate non-current/fixed assets, an auditor not being able to attend the year-end inventory/stock count, and a failure to disclose a contingent liability in the financial statements.

Candidates should also prepare for questions requiring them to define or explain the terms referred to above.

This style of requirement is illustrated in Question 2 from the June 2009 exam paper.

Concluding thoughts

Audit reports are a fundamental part of the auditing process and are therefore significant for audit students at all levels. This will continue to be a regular exam topic.

If you do struggle with these questions it is NOT a good strategy to suggest every possible form of opinion hoping that one of them will be correct.

Auditing requires critical appraisal, the use of professional judgment and the ability to offer a reasoned opinion.

By asking yourself a series of simplified questions you will go through a critical thought process that allows you to come to your own conclusion and, more importantly, offer your own opinion.

This will undoubtedly allow you to present an answer that stands out from the others.

Simon Finley is an audit subject specialist at Kaplan Publishing

Related Links

- Student Accountant hub page

Advertisement

- ACCA Careers

- ACCA Career Navigator

- ACCA Learning Community