The New (and Improved!) New Jersey R&D Tax Credit

New Jersey taxpayers have gotten a long-awaited change to the New Jersey R&D tax credit – specifically an Alternative Simplified Credit method. These changes are effective for tax years beginning on or after January 1, 2018.

New Jersey has offered an R&D tax credit since 1992. The activities qualifying for the credit were based upon the federal rules under IRC Sec. 41. At that time, only the Regular Credit method was established. Therefore, many companies claiming the Alternative Simplified Credit (ASC) method for federal purposes may not have been able to claim a credit in New Jersey. Both credits are only available to corporations.

For more information on the federal R&D tax credit, click here .

The new credit method is calculated similarly to the federal ASC method where the base amount is 50% of the average of the prior three-year qualified research expense (QRE). However, there are differences:

- Where there are no QREs in the prior three tax years, taxpayers still apply the current year QREs against the credit rate of 10%. This is in contrast with the federal calculation where the credit rate drops from 14% to 6% in this scenario.

- The taxpayer must claim the same method (Regular or ASC) for New Jersey as federal.

- A taxpayer CANNOT use the QREs claimed for the federal payroll refund for the New Jersey credit.

- The rationale is that the New Jersey credit is based upon the federal corporate income tax credit. Under The Protecting Americans from Tax Hikes Act of 2015, the payroll refund offset for qualified small businesses was a separate credit under IRC Sec. 3111(f).

- Therefore it will be critical for taxpayers to use the IRS Form 6765 as a starting point on the New Jersey credit.

What this means

- Taxpayers with large revenues were likely not creditable under the previous New Jersey credit regime (Regular method). If they have QREs in New Jersey, they should perform the ASC method to see if creditable.

- If the taxpayer is claiming the federal ASC method, they need to ensure that method is used for New Jersey.

- Many taxpayers are qualified small businesses and claim the payroll offset. Those expenses are not includable in the New Jersey credit calculation.

Click here for form and instructions.

What's on Your Mind?

Timothy Rankins

Tim Rankins is a Tax Director with over 10 years of experience with focus on Research and Development Tax Credit.

Start a conversation with Timothy

Explore More Insights

Reclassification of Marijuana Would Have Significant Tax Impact for Companies

Tennessee Streamlines Tax Code by Repealing Property Measure of Franchise Tax

Generative AI’s Impact on the Tax Practices at Your Organization

- Artificial Intelligence

State Income Tax Opportunities: Tennessee Spotlight

As Bonus Rates Decline, Real Estate Owners Seek Benefit in Other Strategies

SECURE 2.0 Technical Corrections Bill Languishes as a Result of Congressional Inaction

Federal Energy Incentives | 179D Deduction & 45L Credit

How Estate and Tax Law Impact Wealth Planning

Failure to Meet Prevailing Wage Requirements Can Cost You 80% of Energy Credits

Estate and Gift Tax Unified Credit Increase for 2024

COBRA Compliance: Notices

What the Retirement Plan Start-up Cost Tax Credit Means for Healthcare Practice Owners

Receive the latest business insights, analysis, and perspectives from EisnerAmper professionals.

- Our Promise to You

- Success Stories

- Women’s Initiative

- Giving Back

- Appellate Advocacy

- Bankruptcy and Creditors Rights

- Banking and Financial Services

- Banking Litigation and Consumer Finance Defense

- Cannabis, Hemp & Psychedelics

- Construction

- Emerging Markets

- Entertainment

- Environmental

- ERISA and Employee Benefits

- Hospitality Services

- Immigration

- Intellectual Property and Brand Management

- Labor and Employment

- Landlord-Tenant Law

- Life Sciences

- Mergers and Acquisitions (M&A)

- Privacy and Cybersecurity

- Real Estate

- White Collar and Criminal Defense

- Alternative Dispute Resolution

- High Net Worth Divorce

- Personal Injury

- Special Needs

- Trusts and Estates

- Workers’ Compensation

- Professionals

- Other Practice Areas

- Fingerprints on Success Podcast

New Jersey Corporate Income Tax: Revised Timing for Deducting Research and Development Expenditure

In a notable move for businesses operating in New Jersey, the state’s Division of Taxation has recently introduced a new law that affects the timing of tax deductions for research and development (R&D) expenditures. The amendment, which is part of L. 2023, A5323 (c. 96), will impact tax years ending on or after January 1, 2022. Let’s delve into the details of this update and understand how it can benefit corporations in the state.

New Jersey Research and Development Expenditures – Changes in Deduction Timing:

The amended N.J. Rev. Stat. § 54:10A-4(k)(11) introduces a significant change for businesses claiming the Corporation Business Tax Research and Development Tax Credit for New Jersey qualified research expenditures. Starting from January 1, 2022, eligible taxpayers can now deduct their New Jersey expenditures in the same year as they claim the credit. This stands in contrast to the previous requirement, where such expenditures were amortized as mandated by federal tax regulations.

Simplified Recording of Deductions:

With this recent amendment, eligible businesses can benefit from a more straightforward process to record their deductions. They are required to list the relevant amounts as other deductions on Schedule A, Part II of their tax returns. This streamlined approach allows corporations to enjoy more immediate tax benefits for their research and development activities, freeing up resources to reinvest in innovation and growth.

Amended Returns for Improved Deductions:

The new law also provides relief for businesses that had previously amortized their New Jersey qualified research expenditures on their 2022 Corporation Business Tax return. Such taxpayers are allowed to file an amended return, enabling them to take advantage of the revised regulations and avail the benefits of upfront deductions.

Focus on New Jersey Qualified Research Expenditures:

It is important to note that this provision solely pertains to New Jersey qualified research expenditures. For businesses with non-New Jersey qualified research expenditures, the existing deduction rules remain consistent with federal purposes. Consequently, businesses must accurately classify their expenses to ensure they adhere to the appropriate deduction guidelines.

The recent amendment to the timing of New Jersey research and development expenditure deductions holds promising implications for businesses in the state. By allowing upfront deductions for qualified research expenses, the New Jersey Division of Taxation aims to incentivize and support corporate R&D initiatives. This move is expected to stimulate innovation, foster economic growth, and create a more favorable environment for businesses to flourish.

As always, businesses should stay well-informed about tax laws and regulations to optimize their benefits while remaining compliant. Seeking advice from tax professionals can help ensure a comprehensive understanding of the amended rules and their specific implications for each business’s financial situation. By leveraging these tax benefits, corporations in New Jersey can take a stride forward in their pursuit of innovation and prosperity. (Source: Timing of New Jersey Qualified Research Expenditures, N.J. Div. of Taxation, 07/10/2023.)

How can we help you?

* indicates a required field

First Name*

Please leave this field empty.

- Serving US companies nationwide

- Mon - Sun 8am - 6pm CT

- (512) 503-3080

- What is the R&D Tax Credit?

- What qualifies for a Research and Development Tax Credit?

- How can your business benefit from the R&D tax credit?

- How can my business claim an R&D Tax Credit?

- Common misconceptions why businesses assume they don’t qualify for the R&D Tax Credit

- What states qualify for the R&D Tax Credit?

- How to determine your R&D Tax Credit eligibility?

- Research and Development Tax Credit Limitations

- R&D Tax Credit Examples

- Research and Development Tax Credit Calculation – How to calculate your R&D Tax Credit

- What documentation is required to claim an R&D Tax Credit?

- How has the R&D Tax Credit Changed in Recent Years?

- How has tax reform changed the R&D Tax Credit in recent years?

- What are the R&D Tax Credit Costs?

- When Did R&D Tax Credits Start?

- R&D Tax Credit Carryforward

- How do Tax Credits Work?

- When can you Claim R&D Tax Credit?

- What is IRS Form 6765?

- How can an R&D Tax Credit Offset Payroll Taxes?

- R&D Tax Credits for Small Businesses & Startups

- R&D Tax Credit FAQ (Frequently Asked Questions)

- Employee Retention Credit

- Connecticut

- North Dakota

- Pennsylvania

- Rhode Island

- South Carolina

- Massachusetts

- Mississippi

- New Hampshire

- South Dakota

- West Virginia

- Aerospace Engineering R&D Tax Credits

- Aviation R&D Tax Credits

- Firearms, Ammunition & Heavy Weapon Defense R&D Tax Credits

- Government Contractors R&D Tax Credits

- Jet Propulsion & Rocketry R&D Tax Credits

- Space Exploration R&D Tax Credits

- Satellite Technology R&D Tax Credits

- Agricultural & Farming R&D

- Craft Brewery R&D Tax Credits

- Distillery R&D Tax Credits

- Hard Seltzer R&D Tax Credits

- RTD (Ready to Drink) Cocktail R&D Tax Credits

- Winery (Vineyards) R&D Tax Credits

- Architecture R&D Tax Credits

- Civil Engineering R&D Tax Credits

- Construction Engineering R&D Tax Credits

- Electrical Engineering R&D Tax Credits

- Environmental Engineering R&D Tax Credits

- LEED/Sustainable Architecture R&D Tax Credits

- Mechanical Engineering R&D Tax Credits

- Structural Engineering R&D Tax Credits

- Analytic Research Laboratories R&D Tax Credits

- Clinical Trials R&D Tax Credits

- Compounding R&D Tax Credits

- Generic Drug Development R&D Tax Credits

- Medical Devices R&D Tax Credits

- Medical Equipment Manufacturers R&D Tax Credits

- Orphan Drug Development R&D Tax Credits

- Packaging R&D Tax Credits

- Pharmaceutical Development & Reformulation R&D Tax Credits

- Reagent Development R&D Tax Credits

- Vaccine R&D Tax Credits

- Meat & Seafood Processing R&D Tax Credits

- Packaged Foods R&D Tax Credits

- Plant-Based Business R&D Tax Credits

- Dairy Processing R&D Tax Credits

- Co-Packing R&D Tax Credits

- Frozen Foods R&D Tax Credits

- Industrial Hemp R&D

- Apparel & Textiles R&D Tax Credits

- Automotive & Original Equipment Manufacturers (OEMs) Tax Credits

- Chemical Company R&D Tax Credits

- Electronics R&D Tax Credits

- Food & Consumer Packaging R&D Tax Credits

- Industrial Automation R&D Tax Credits

- Metals & Alloy Manufacturing R&D Tax Credits

- Oil & Gas R&D Tax Credits

- Plastic Injection Molding R&D Tax Credits

- Robotics Manufacturing R&D Tax Credits

- Semiconductor R&D Tax Credits

- Shipbuilding & Marine Manufacturing R&D Tax Credits

- Tool & Die Manufacturing R&D Tax Credits

- Artificial Intelligence R&D Tax Credits

- Blockchain R&D Tax Credits

- Cryptocurrency R&D Tax Credits

- Electronics (Technology) R&D Tax Credits

- FinTech R&D Tax Credits

- Robotics (Technology) R&D Tax Credits

- Telecommunications R&D Tax Credits

- Video Game Development R&D Tax Credits

- VR/AR Development R&D Tax Credits

Contact us for a free R&D tax credit assessment and quote

Looking for a First-Class R & D tax credit advisor?

New Jersey R&D Tax Credit

Businesses today invest heavily in research and development to remain competitive in an increasingly digital global economy. However, many companies don’t have the resources or cash flow to fund these programs from their own operating capital. As a result, they are at a disadvantage when meeting international standards for innovation and growth.

Fortunately, state lawmakers understand that without funding assistance, such businesses may not be able to invest in new R&D programs. For this reason, legislators have created tax credits for R&D programs across the US. New Jersey R&D tax credit is an incentive for businesses in the area to continue growing and expanding at home instead of moving overseas or shutting down completely.

New Jersey Research and Development Tax Credit Explained

New Jersey research tax credit has undergone significant modifications that affect tax years starting from 2018. In general, it equals ten percent of the extra QREs above the basic amount. The state follows the federal description of QREs (you can check it in IRC Section 41. (b) ).

You can also utilize the alternative simplified method to calculate incentives for taxable years that end on or following July 31, 2019. But that method only applies to consolidated groups, so you must be a part of a combined group that is included on an NJ combined return .

In contrast to its federal counterpart, the New Jersey research tax credit is solely available to C-corporations and some qualified S-corporations. Moreover, stockholders cannot receive any credits.

Unused credits typically have a 7-year carryforward window. However, credits closely connected to specific industries have a 15-year carryover duration. They include medical device technology, environmental technology, electronic device technology, biotechnology, advanced materials, and advanced computing industries.

How to Calculate New Jersey R&D Tax Credit

Take ten percent of the surplus of QREs for the taxable year above the base amount, then add ten percent of basic research costs for the taxable period. Moreover, New Jersey started allowing the ASC method to compute credits on January 1, 2018, but there won’t be Code 280C compliance.

Claiming the Federal Payroll Tax Credit

The permissible payroll credit under IRC Sections 3111(f) and 41(h)(1) and the corporate income tax credits under IRC Section 41(a) are different incentives. The federal corporate income tax credit is the foundation for the NJ Corporation Business Tax R&D Tax Credit. For this reason, the NJ research tax credit doesn’t cover such costs, and you shouldn’t use them to calculate the final amount.

New Jersey Research and Development Tax Credit: Takeaway

If you own an S-Corp in New Jersey, you are eligible for a credit relating to expanding your research operations to the extent of your NJ corporation tax burden. But you can’t pass it on to the shareholders.

What kind of companies can apply for an R&D tax credit in New Jersey?

C-Corporations

What is the deadline for applying for an R&D tax credit in New Jersey?

You must submit your application together with the New Jersey Tax Return.

What data do I need to calculate credit an R&D tax credit in New Jersey?

Gross receipts for the past four years, New Jersey QREs for the past three years, as well as claim period New Jersey QREs (Qualified R&D Expenses).

What information do I need to provide to file an R&D tax credit in New Jersey?

Federal Form 6765

Is credit carryforward an option in New Jersey?

Yes, up to seven years or fifteen years for certain industries.

R&D Tax Credits by State:

Alaska research and development tax credit Colorado research tax credit Connecticut research and development tax credit Michigan research and development tax credit Nebraska research tax credit California research tax credit Kansas research tax credit Ohio R&D tax credit Utah research and development tax credit Massachusetts research and development tax credit

Texas research and development tax credit Mississippi research and development tax credit New Mexico R&D tax credit Louisiana research and development tax credit Vermont R&D tax credit Pennsylvania R&D tax credit Virginia research and development tax credit Georgia research tax credit Hawaii R&D tax credit Rhode Island R&D tax credit

South Carolina research and development tax credit Indiana research and development tax credit Maryland research and development tax credit Arizona R&D tax credit Maine research tax credit Alabama R&D tax credit New Hampshire R&D tax credit Illinois R&D tax credit Arkansas research tax credit Kentucky research tax credit

New Jersey research tax credit Iowa research and development tax credit North Dakota research tax credit Florida R&D tax credit Delaware research tax credit Minnesota research tax credit New York research and development tax credit Idaho R&D tax credit Wisconsin research and development tax credit

Income/Franchise: New Jersey: New Bulletin Addresses Conformity with IRC §174 and Recent R&D Credit Law Changes

Tax Bulletin No. TB-114: The New Jersey Research and Development Tax Credit , N.J. Div. of Tax. (12/22/23). A newly posted New Jersey Division of Taxation (Division) bulletin explains certain aspects of research performed in New Jersey and related issues for both New Jersey corporation business tax (CBT) and gross (individual) income tax purposes as it relates to the CBT’s research and development (R&D) tax credit and the gross income tax deduction for qualified research expenditures and payments. The bulletin reflects legislation enacted in 2023 that made significant changes to the CBT [see A.B. 5323 (2023) and previously issued Multistate Tax Alert for more details on these law changes], including how while New Jersey generally conforms to the current version of the Internal Revenue Code (IRC) and follows the federal Tax Cuts and Jobs Act of 2017 changes to IRC section 174(a)(2)(B) for privilege periods beginning on or after January 1, 2022, taxpayers that claim the CBT R&D tax credit for New Jersey qualified research expenditures can also deduct those New Jersey expenditures on their tax return in the same year as they claim the credit, rather than amortizing the expenditures as required by IRC section 174. Please contact us with any questions.

R&D Tax Credits

R&d tax credits.

Small business survival and growth requires adequate working capital. One overlooked source of cash for New Jersey manufacturers is the Research and Development (R&D) tax credit. This incentive helps companies to grow by reducing its tax liability for qualified R&D expenditures.

Most manufacturers are unaware that their efforts in designing quality products qualify as R&D, and may make them eligible for tax credits for expenditures associated with these activities . R&D credits may be applied to taxes due or to future tax liability, and they may be retroactive for three years in addition to the current year and carry forward for twenty years! These credits can additionally be used to reinvest in the company.

NJMEP’s Process

NJMEP’s experts have experience identifying, qualifying and quantifying the expenditures of manufacturers. Areas of analysis include:

- Salaries and wages of the engineers working on a project

- Cost of supplies

- Third party contractor fees getting prototype parts made by a rapid prototyping service center

- Tasks performed by executive leadership

- Legal, sales engineers, operations and IT

Click here or call us at 973-998-9801 for more information, or fill out the form below!

" * " indicates required fields

Request Your Complimentary Assessment

Schedule Now

Subscribe to Newsletter

Subscribe to the NJMEP Newsletter to receive our latest updates.

Official Site of The State of New Jersey

- FAQs Frequently Asked Questions

The State of NJ site may contain optional links, information, services and/or content from other websites operated by third parties that are provided as a convenience, such as Google™ Translate. Google™ Translate is an online service for which the user pays nothing to obtain a purported language translation. The user is on notice that neither the State of NJ site nor its operators review any of the services, information and/or content from anything that may be linked to the State of NJ site for any reason. - Read Full Disclaimer

- Search close

Division of Taxation

The newark and somerville regional information centers will be permanently closed as of may 9, 2024. these regional information centers will be merging and relocating to our new cranford location. our new office is not open yet, but will be soon. check back online for more details. for in-person assistance during this timeframe, you may visit one of our other regional information centers ., timing of new jersey qualified research expenditures.

P.L. 2023, c. 96, signed into law on July 3, 2023, amended N.J.S.A. 54:10A-4(k)(11) for privilege periods beginning on and after January 1, 2022. Taxpayers that claim the Corporation Business Tax Research and Development Tax Credit for New Jersey qualified research expenditures can also deduct those New Jersey expenditures on their tax return in the same year as they claim the credit, rather than amortizing the expenditures. Taxpayers will record these amounts as "other deductions" on Schedule A, Part II. Taxpayers that amortized their New Jersey qualified research expenditures on the 2022 Corporation Business Tax return can file an amended return.

N.J.S.A. 54:10A-4(k)(11), which requires an addback of certain qualified research expenditures, only applies to New Jersey qualified research expenditures . Non-New Jersey qualified research expenditures are deductible in the same manner and with the same timing as they are for federal purposes. Thus, if you added back your non-New Jersey qualified research expenditures, you should file amended returns for years still within the statute of limitations.

Cannabis Licensees. P.L. 2023, c.50 decoupled the corporation business tax and gross income tax from the federal provisions that prohibit tax credits and deductions for cannabis businesses. However, it is applicable to tax years beginning on and after January 1, 2023 so these licensees are only eligible to utilize the amendment to N.J.S.A. 54:10A-4(k)(11) prospectively. See TB-106 for more information.

Get Your Free Assessment (561) 257-3436

New jersey state r&d tax credit, refundable tax credit – yes.

Businesses can take advantage of the Research and Development Tax Credit in the state of New Jersey. Companies can use the credits to offset costs spent performing qualifying research activities against state and federal tax liabilities. The credit is often overlooked by companies simply because they don’t realize the work they are doing in their daily operations qualifies them. Companies performing any kind of research and development may be missing out on significant tax credits.

Businesses in New Jersey can take advantage of the federal R&D Tax credit, as well as credits specific to the state of New Jersey.

New Jersey State R&D Tax Credit Program Highlights

- Unused credits can be carried forward up to 7 years

- The credit is equal to 10% of the excess of the qualified research expenses for the tax period over the base amount, plus 10% of basic research payments for the tax period.

- Qualifying expenditures that have been made in taxable years since 1993 can take advantage of the credit.

- An R&D tax credit against the entire net income component of the corporation business tax is allowed for qualifying research activities performed in New Jersey.

Federal R&D Tax Credit Program Highlights

- Every year, more than $7.5 billion in federal R&D credits are given out to companies across the United States.

- The Research and Development Tax Credit provides cash incentives through the form of credits for companies performing research activities in the United States.

- The credit offsets cost spent performing research activities against federal tax liabilities.

- Tax credits may be carried forward as far as 20 years.

- The credit can be taken by a business on all open tax years, typically the last three or four years, plus the current year.

- The credit creates a significant reduction to current and future federal tax liabilities.

- All companies can potentially benefit from the tax credit if qualifying research activities are taking place.

The Research and Development Tax Credit

R&D is a dollar for dollar tax credit that can be claimed by companies in the United States to offset costs spent performing research and development to benefit their business. Created as an incentive by the United States Government for businesses to undergo research activities to develop or improve their products, processes, or software, The R&D credit was made permanent on a federal level by the Protecting Americans Against Tax Hikes Act of 2015, allowing business owners to ensure their research activities would earn them the lucrative credit. The PATH Act also broaden the variety of industries that are able to claim the credit.

How to Apply

Claiming your R&D tax credits is made simple by our team at National Tax Group. During your call, we’ll determine if your research activities qualify your company to take advantage of the R&D Tax Credit Program. We’ll provide the proper documentation and remain by your side until all documentation is submitted and approved by the Internal Revenue Service. In the highly unlikely event of an audit, we will supply all materials needed to clear it at no extra cost for you. Contact our tax experts to get started.

New Jersey R&D Tax Credits

Connect with us to find out how R&D tax credits can boost your organization’s bottom line.

New Jersey R&D Tax Credit

Discover the benefits of New Jersey state credits and see how your business could qualify.

There have been major changes to the New Jersey R&D Credit that are prospective only for tax periods beginning on or after January 1, 2018. The New Jersey R&D credit provides a credit roughly equal to 10% of the excess of qualified research expenses over the base amount.

New Jersey mirrors the federal definition of QREs, as defined by IRC § 41(b). For tax years ending on or after July 31, 2019, taxpayers should use the Federal rules for computing the New Jersey R&D Credit that are applicable to consolidated groups if the taxpayers are a taxable member of a combined group included on a New Jersey combined return.

Unlike the Federal R&D credit, the New Jersey R&D credit is only applicable for qualifying C-Corps and in rare circumstances S-Corps. However, no credits can be passed through to shareholders.

There is generally a 7 year carryforward period for unused credits. Alternatively, there is a 15 year carryforward period for credits directly tied to projects involving specific study fields (see below).

Learn more about New Jersey's R&D Tax Credit law from Form 306.

R&D Tax Credit Available:

Eligible Entities:

C-Corporations

Deadline for Tax Filing:

Due with New Jersey Tax Return

Data Required to Compute Credit:

Claim Period New Jersey Qualified R&D Expenses (QREs)

Prior 4 years of Gross Receipts

Prior 3 years of New Jersey QREs

What Information is needed?

Federal Form 6765

Credit Carryforward:

15 years for specific industries (see below)

The R&D tax credit equals:

10% of the excess of the NJ qualified research expenses for the tax period over the base amount; plus

10% of basic research payments for the tax period.

Specific Items to Note:

Effective Jan 1, 2018, New Jersey allows the alternative simplified method (ASC) to calculate the state credit, however there is no Section 280C conformity.

The standard carryforward period for New Jersey R&D credits is 7 years; however, companies in the following industries can carry forward any unused R&D credit up to 15 years:

- Advanced computing;

- Advanced materials;

- Biotechnology;

- Electronic device technology;

- Environmental technology; and

- Medical device technology.

A New Jersey S-Corporation is allowed to claim a credit in connection with increasing research activities to the extent of its New Jersey corporation tax liability. Pass-through of this credit to shareholders is not permitted.

For Federal Payroll Tax Credit Claims : Pursuant to I.R.C. § 41(h)(1), the corporate income tax credit under I.R.C. § 41(a) and the allowable payroll credit under I.R.C. § 41(h)(1) and § 3111(f) are separate and distinct credits. The New Jersey Corporation Business Tax Research and Development Tax Credit is based on the federal corporate income tax credit. These expenses may not be used for the New Jersey R&D credit. Do not use these amounts in the above calculation of the New Jersey credit.

Estimate the value of your NJ R&D tax credits!

New jersey r&d tax credit eligibility summary:, new jersey r&d tax credit guidelines:, new jersey r&d tax credit case study, key new jersey r&d tax credits r&d tax rules changes.

Check New Jersey R&D Tax Credit Law

Connect with us to find out how R&D Tax Credits can boost your organization’s performance.

With just a little info, our Strike Experts can help you start your R&D tax credit journey.

What’s a Rich Text element?

The rich text element allows you to create and format headings, paragraphs, blockquotes, images, and video all in one place instead of having to add and format them individually. Just double-click and easily create content.

Static and dynamic content editing

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

How to customize formatting for each rich text

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.

Ready to calculate your R&D tax credits?

To get an estimate of the potential value of your unclaimed R&D Tax Credits, try out our credit calculator.

Download our R&D Tax Credit Calculator for Android to see how much you can receive from your qualified R&D tax credit expenses.

Can I Claim R&D Tax Credits in New Jersey?

Yes, you can claim R&D tax credits in New Jersey. The state offers a research and development tax credit program known as the Research and Development Tax Credit.

The Research and Development Tax Credit (R&D) is a tax credit designed for businesses, regardless of their size, engaged in research and development activities in the United States. This tax credit has a broad application, encompassing a wide range of businesses and industries, extending far beyond the realm of scientists and research laboratories. The R&D tax credit was established to encourage research and development efforts undertaken in the United States. Over time, an increasing number of companies have been capitalizing on this tax credit. Furthermore, in 2015, the Protecting Americans from Tax Hikes (PATH) Act made the R&D tax credits permanent, providing startups with the opportunity to reap its benefits as well.

What are the Potential Benefits of the R&D Tax Credit?

Claiming R&D tax credits can lead to substantial cost savings for eligible companies. These benefits include:

- Increasing Cash Flow

- Federal and State Dollar-for-Dollar Income Tax Reduction

- Claim Credits for Open Tax Years Going Back 3-4 Years

- Reducing Your Tax Rate

$1.6 BILLION

Who can claim the r&d tax credit.

R&D tax credits are not limited to lab coat-wearing inventors and groundbreaking products. They are actually far broader and more inclusive than most people think.

Many companies, regardless of size or industry, are eligible for Research and Development (R&D) Tax Credits from the federal government. However, a large number of these companies are unaware of their eligibility. This means they are missing out on significant financial benefits from both federal and state R&D tax credits.

Many companies, regardless of their size or industry, are eligible for Research and Development (R&D) Tax Credits offered by the federal government. Unfortunately, a large number of these companies are unaware of their eligibility and miss out on substantial financial benefits. Numerous businesses are leaving money behind by not taking advantage of both federal and state R&D tax credits that they are entitled to.

The activities that qualify for the R&D tax credit directly contribute to the growth of your business.

- Developed new products

- Improved existing products

- Developed software for internal or external use

- Improved manufacturing processes

The activities that qualify for the New Jersey R&D tax credit are the same ones driving growth in your business.

How do i claim the r&d tax credit.

On average, companies can usually claim a federal R&D tax credit amounting to 7-10% of their eligible expenses. For instance, a software developer, engineer, or lab technician with an annual W2 income of $100,000 may realize tax savings of up to $10,000.

Expenses eligible for research activities within your company typically encompass employee compensation, materials, and contracted services. There are several types of documentation that can substantiate these qualified expenses, such as payroll records, financial records indicating supply or contract research expenditures, and vendor invoices.

R&D Tax Credit

Our platform, partner with us, news & blog, cookie consent.

ICS Tax, LLC

Helping New Jersey Taxpayers With the Research & Development Tax Credits

R&D TAX CREDIT: NEW JERSEY

The Research and Development (R&D) tax credit is a Federal tax incentive that rewards taxpayers for increasing investment in U.S.-based research activities. The R&D tax credit is available to businesses that uncover new, improved or technologically advanced products, processes, principles, methodologies or materials. In addition to “revolutionary” activities, the credit may also be available if the company has performed “evolutionary” activities such as investing time, money and resources toward improving its products and processes.

The R&D tax credit is primarily a wage-based credit, which is worth approximately 6.5% of qualified R&D activities. Thus, a taxpayer with $1M of qualified wages could receive a $65,000 benefit. Many states, including New Jersey, also offer R&D tax credit that can greatly enhance the value of the study. Further, the credit can often be claimed for prior tax years.

HOW WE HELP NEW JERSEY TAXPAYERS

ICS Tax can prepare all necessary documentation to support the credit, calculate both the Federal and the New Jersey credit amount, and draft necessary compliance. In the event of an IRS audit, we can help support your credit.

ICS Tax, LLC (ICS) is a consulting firm providing innovative tax planning strategies. ICS collaborates with taxpayers and their tax professionals to identify credits and incentives that reduce tax liabilities and increase profitability. We serve Newark, Jersey City, Paterson, Elizabeth, Edison and all other cities within New Jersey and throughout the nation.

PROPOSAL REQUEST

Meet your expert team.

Regional Director

Join us at one of our events. Register Today

- Newsletters

- Client Portal

- Make Payment

- (855) Marcum1

Services Search

Research & development tax credit, the r&d tax credit can apply to businesses in multiple industries - don’t miss out.

- Tax Advisory Services

- Tax Credits & Incentives

- Research & Development Tax Credit

The Research and Development Tax Credit is often overlooked, but it can provide enormous benefits to companies that recognize its potential. Typically, organizations claim less tax benefit than they’re entitled to or, even worse, believe they don’t qualify because research and development isn’t their main business. In addition to the federal tax credits, many states have enacted generous credit programs, and some are refundable even if you haven’t paid taxes.

Marcum has helped our clients save more than $200 million using the Research & Development Tax Credit.

How can credits benefit your company?

- Provide cash refunds of previously paid federal and state taxes.

- Reduce your current federal and applicable state tax expense.

- Free up capital for investment in business, product development, and debt reduction.

- Increase the value of your business to potential buyers or investors.

- Provide Alternative Minimum Tax (AMT) relief.

- Deliver a payroll tax expense refund/reduction.

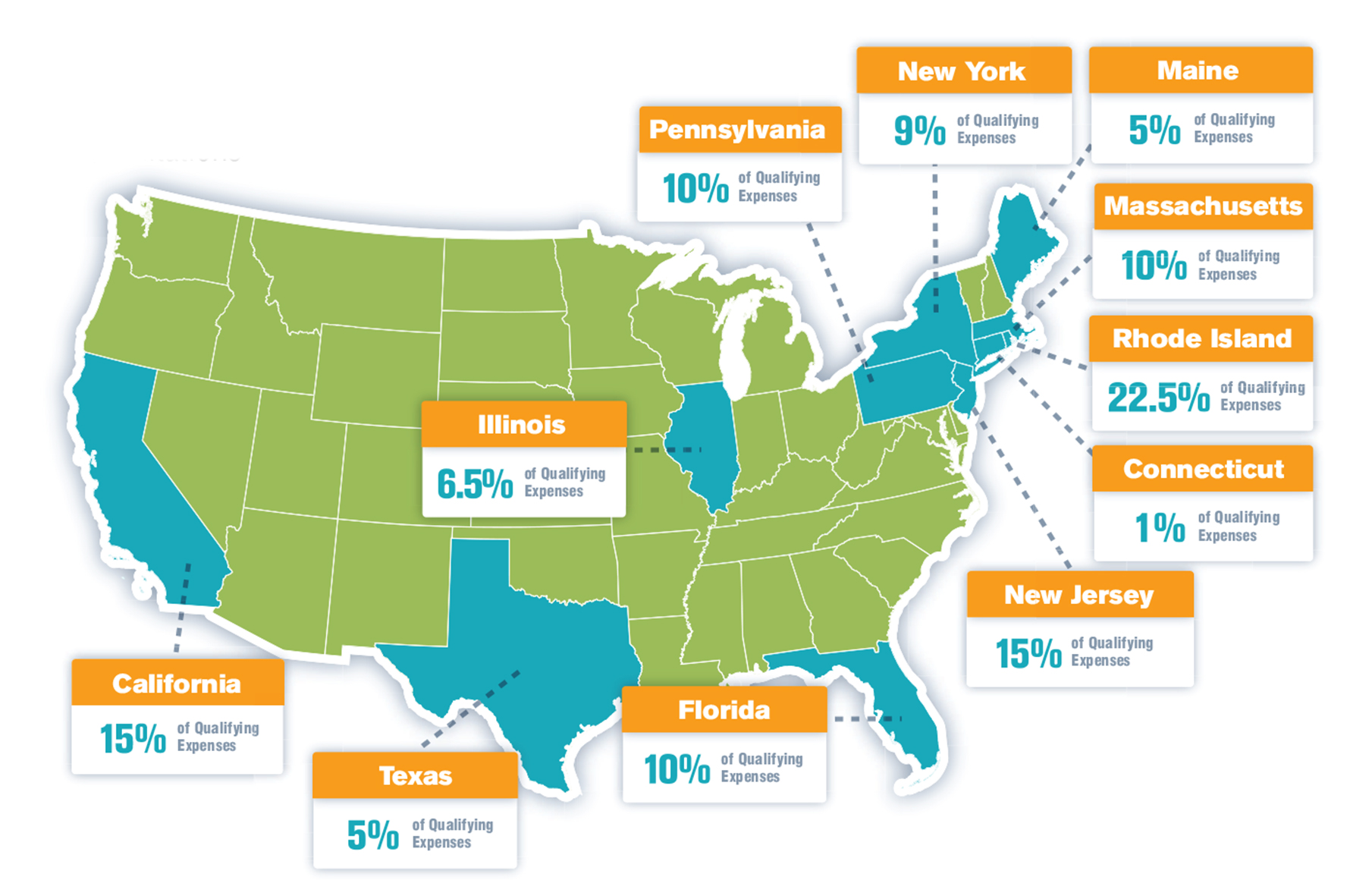

R&D Credits Available in Marcum Office Regions*

*States have unique qualifying limitations.

Industries where we’ve helped clients claim the credit

- Business and Professional Services

- Construction

- Consumer Products (Food & Beverage, Cannabis, Retail & Apparel, Arts & Entertainment)

- Financial Services (Fintech, Alternative Investments, Broker/Dealer, Financial Institutions, Insurance)

- Manufacturing & Distribution (Energy & Utilities, Manufacturing/Wholesale/Distribution, Transportation)

- Private Equity

- Technology & Life Sciences (Data & Analytics, Software Development)

What types of activities qualify?

- Investing in resources for new or improved products.

- Investing to develop new or improved manufacturing or service processes.

- Investing in software and software-related technology – i.e., Artificial Intelligence, financial modeling, fin-tech applications, security protocols, and more.

- Efforts to improve manufacturing efficiency, reduce scrap, and implement techniques like “lean,” “green,” “Kaizen,” and “Kanban.”

- Owning existing patents or patents pending.

Marcum Year-End Tax Guide

Tax planning for 2023 and 2024, insights & news.

Seize the Opportunity: NYC’s Biotechnology Tax Credit Back in Action

New Jersey Cool Program Offers Financial Support for Eco-Friendly Retrofits in Commercial Buildings

Marcum LLP Unveils Comprehensive 2023 Year-End Tax Guide

Research and Development: Tax Credit Benefits and Capitalization Considerations

IRS Unleashes New Era for Green Projects: How to Capitalize on Transferable Tax Credits

Status of Section 174 Capitalization Legislation – The Build It in America Act

The Inflation Reduction Act Sparks Green Revolution in Real Estate Development with Billions in Tax Breaks

The Wall Street Journal interviewed Partner William Kuhlman, national R&D Tax Credits leader, for an article about how a change in deduction rules is impacting small businesses.

Partners Barry A. Fischman and William R. Kuhlman wrote about how changes to Research and Development expense rules impact contractors, for Surety Bond Quarterly.

The Inflation Reduction Act May Be Worth a Drive

Leveraging the Prevailing Wage and Apprenticeship Requirements of the Inflation Reduction Act

Giving Pennsylvania an EDGE with Credits and Incentives

Select the region to view contacts.

- All Offices

- Connecticut

- Pennsylvania

William Kuhlman

R&d tax credits leader.

- Tax & Business

- Philadelphia, PA

Peter Downing

National principal-in-charge, tax credits & incentives.

- Costa Mesa, CA

John Eckweiler

Barry Fischman

- New Haven, CT

Diane Giordano

- Melville, NY

James Lundy

- Nashville, TN

Partner-in-Charge, Healthcare Tax Services

- Deerfield, IL

Jeffrey Winkleman

Partner-in-charge, corporate taxation, have a question ask marcum.

- ATLANTIC HIGHLANDS

- LITTLE SILVER

- MONMOUTH BEACH

- TINTON FALLS

- PEOPLE PAGES

- Sign in / Join

Netflix Solidifies New Jersey Partnership

On Monday, a source close to Netflix told The Two River Times that the fort’s McAfee Center, a 1997 technology development building, will be among the first to be adaptively reused. The structure, named for Dr. Walter S. McAfee, a civilian engineer who worked on pivotal projects there, will become office space for productions filming on the studio lot with support space dedicated to wardrobe, hair and make-up, and dressing rooms.

RELATED ARTICLES MORE FROM AUTHOR

Women Take the Reins as New Generation of Jockeys, Trainers at Monmouth Park

Red Bank Planning Board Considers Cannabis Dispensary: CoCo Parì to Become a Café

Editor picks.

5 Questions for Shrewsbury Mayor Erik Anderson

How to Get Married During a Pandemic? With Tents, Masks and...

Fort Monmouth 2021 Forecast

Popular posts.

Sign Up and Line Up: Vaccines Are Here

Riverside Marina Restaurant Reopens Featuring Mystic Lobster, New Menu

Hundreds Turn Out for Red Bank March for Justice

Women Take the Reins as New Generation of Jockeys, Trainers at...

The Buzz About Summertime Bee Lawns

Popular category.

- Obituaries 3381

- Top News 2234

- Lifestyles 1486

- Sports 1028

- Entertainment 946

- Business 661

- Letters & Commentary 637

- Opinion 578

- CLASSIFIEDS

- SCENE PAGES

- OUR NEWSLETTER

- FIND THE PAPER

- EMPLOYMENT OPPORTUNITIES

KEEP IN TOUCH

Sign up to The Two River Times newsletter.

You have successfully subscribed to the newsletter

There was an error while trying to send your request. Please try again.

NJEDA.com contains a link to translation services provided by Google™ Translate, a free online translation service. Google™ Translate is subject to its own terms of service, which can be viewed at ( https://policies.google.com/?hl=en ). The link does not constitute affiliation, endorsement, support, or approval of Google™ Translate.

Neither the NJEDA nor the State of New Jersey (collectively, the “State”) reviews the services, information or content provided by Google™ Translate. Information translated by Google™ Translate may not be accurate or current and is used at the user's sole risk. The NJEDA has no obligation to offer translation, and this service could change or be discontinued at any time.

The State expressly and fully disavows and disclaims any responsibility or liability in respect to any cause, claim, or consequential or direct damage or loss, however described, arising from the use of Google™ Translate.

NJEDA.com is provided "AS-IS" with no warranties, express or implied, and its use confers no privileges or rights.

For additional language assistance, please click here to contact NJEDA to request assistance.

New NJEDA Funding Program for Cultural Arts Facilities in New Jersey

Related events.

Registrarse como empresa y obtener su certificado de liquidación de impuestos

Info session: registering as a business and getting a tax clearance certificate, info session: activation, revitalization, and transformation (a.r.t) program, webinar: grant opportunities from njif and csit, nurturing the future: innovations in maternal and infant health, emerging developers grant program information session – atlantic city, tax credit auction info session – food desert relief, info session: atlantic city food security pilot grants program, njeda emerging developers grant program webinar, trenton info session: emerging developers grant program, camden info session: emerging developers grant program, in-person njeda resource fair: show me the resources, new jersey manufacturing voucher program (njmvp) – phase 2 information session, info session: njeda atlantic city revitalization grant program, application walkthrough: food desert supermarket initial operating cost tax credit program, info session: new jersey local property acquisition grant program, njeda cannabis equity grant program webinar: seed equity grant, celebrating hispanic-owned businesses with njeda and partners, njeda film & digital media studio infrastructure program – info session, welding & painting job opportunities in paulsboro, open office hours with njeda and the new activation, revitalization, and transformation (art) program, cannabis equity grant program webinar: seed equity grant, njeda property acquisition redevelopment fund listening and information session, 2023 governor’s conference on housing and economic development, new jersey economic development authority’s (njeda) activation, revitalization, and transformation (art) program overview, njeda brownfields redevelopment incentive program information session, njeda food retailer innovation in delivery grant (fridg) application overview, njeda small business week: show me the resources webinar for central/south new jersey, njeda small business week: show me the resources webinar for northern new jersey, semana nacional de la pequeña empresa de la njeda: ¡muéstrame los recursos, njeda hosts: atlantic city business town hall, njeda construction inflation fund information session, public listening session: food desert tax credit program, public listening session: food desert tax credit program, njeda child care facilities improvement program- information session for nj contractors, njeda offshore wind workforce and skills development grant challenge – info session, njeda’s food security planning grant roll out, njeda’s main street micro business loan – info session, public listening session: njeda’s brownfield redevelopment incentive program, child care facility improvement program – njeda funding information session, njeda historic property reinvestment incentives for government restricted municipalities.

2022 GOVERNOR’S CONFERENCE ON HOUSING AND ECONOMIC DEVELOPMENT

Njeda historic property reinvestment program – eligibility, requirements & how to apply, njeda’s aspire program – gap financing help for developers, sustain and serve nj grant program – phase 3 application overview, 2022 nj planning and redevelopment conference, aaccnj – circle of achievement awards gala, food desert communities – njeda & dca listening session, food desert communities – njeda listening session, njeda listening session: historic property reinvestment program, main street recovery finance program listening session – atlantic city, main street recovery finance program listening session – paterson, main street recovery finance program listening session – trenton, northeast sustainable communities workshop: opportunities abound.

- Gov + Legislature

- Criminal Justice

- Social Justice

- Election 2024

Senate panel approves changes to tax incentive program

By: nikita biryukov - may 16, 2024 5:17 pm.

Bill sponsor Sen. Nellie Pou said the state’s Aspire tax incentive program has helped to revitalize communities by offering tax credits for mixed-use, transit-oriented development. (Dana DiFilippo | New Jersey Monitor)

A Senate panel has unanimously approved a bill that would require some recipients of certain state tax incentives to temporarily cede their awards if occupancy falls too low and allow the Economic Development Authority to extend loans meant to fill funding gaps that tax credits do not.

The bill , which the Senate Economic Growth Committee approved in a unanimous vote Thursday, would be the latest update to the voluminous Aspire tax incentive program signed into law in 2021, one meant to encourage development, including in some of the state’s most beleaguered cities.

“We all know of successes the Aspire program has realized in its short lifespan. It has offered unique opportunities that have helped revitalize communities by offering supports to mixed-use, transit-oriented and real estate development through tax credits that help to close financing gaps,” said bill sponsor Sen. Nellie Pou (D-Passaic).

Among a host of other changes, the bill would require commercial projects to maintain at least 60% average occupancy within a given tax year beginning three years after the project receives a final certificate of occupancy. Those who fail to maintain occupancy at that level would be required to forfeit their tax credits and could not reclaim them until they brought average occupancy back up to 60%.

The provision is meant to send more workers to physical office buildings and the shops that surround them. In part, the state’s tax incentive programs are intended to boost economic activity in disadvantaged towns and cities, a mission made harder by the rise of remote work.

The legislation would create new incentives to redevelop abandoned commercial buildings, allowing the Economic Development Authority, which administers tax incentives under Aspire and related programs, to raise awards by up to 10% of a project’s total cost.

“I’m here today before you because we are at a precipice in the commercial real estate industry in this country with regards to a number of office buildings that are being devalued because of the lack of revenue because of the new normal for working,” said Tony Pizzutillo, a government affairs consultant for NAIOP, a commercial real estate development association.

The bill would allow smaller enhancements — 5% and 3% of project costs, respectively — to residential projects where three-bedroom units account for at least 20% of low- and moderate-income units or to projects that hire local workers.

Tax credits from any source could cover no more than 80% of a project’s costs, or 90% if the project receives credits through the federal Low-Income Housing Tax Credit Program.

Some questioned the need for more generous terms on tax incentives.

“What is the problem this is actually trying to solve? Whenever there’s some huge tax credit bill that has lots of changes in it, you’ve got to wonder what is the problem here?” Peter Chen, a senior policy analyst for New Jersey Policy Perspective, told the Monitor. “There’s already a decent number of Aspire programs. There’s lots of projects that have been funded.”

Other provisions would allow the Economic Development Authority to issue bridge loans in cases where tax credits do not fully fill funding gaps and loans would enable project completion. The authority could issue loan guarantees under the same terms.

The bill would allow developers to propose terms for loans or guarantees through the agency, but the legislation would give ultimate authority on terms to the EDA.

Proceeds from the loans would go back into a revolving fund from which the loans would be issued. Within 90 days of the bill’s enactment, the EDA must recommend an initial appropriation for the revolving fund, though the size of that appropriation is yet unclear.

Other provisions would allow the state treasurer to redeem outstanding tax credits at a discount of not more than 10%. Developers would receive the outstanding value of the credit as a tax refund over one or more years.

Existing law allows the Treasury to recoup unused tax incentives, paying no more than 75% of their value, with some exceptions.

Though the bill met with little opposition Thursday, one hesitant supporter urged caution on provisions that would allow developers to skirt community benefit requirements tied to most awards under Aspire.

“As it’s currently constructed, that certification with the municipalities could end up being a problematic portion,” said James Williams, director of racial justice policies and government relations for the Fair Share Housing Center.

In nearly all circumstances, developers that receive awards under Aspire are required to enter agreements with the host town to offer job training, employment, youth development, and similar services.

Existing law allows developers to meet community benefit requirements if the host municipality certifies certain documents, but developers who do so must be overseen by a community advisory committee and certify they are providing the benefits they agreed to or risk losing tax credits.

The bill would exempt developers from that oversight if the host municipality adopts the same documents through a resolution.

“If the whole purpose of this is ‘these have benefits to the community,’ then it should be relatively easy to develop something that says ‘this actually has benefits to the community’ rather than just an elected body essentially just certifying that, ‘yep, it sure does have benefits’ and moving on,” Chen said.

Appropriation committees in both chambers must approve the legislation before it reaches a floor vote.

SUPPORT NEWS YOU TRUST.

Our stories may be republished online or in print under Creative Commons license CC BY-NC-ND 4.0. We ask that you edit only for style or to shorten, provide proper attribution and link to our website. AP and Getty images may not be republished. Please see our republishing guidelines for use of any other photos and graphics.

Nikita Biryukov

Nikita Biryukov is an award-winning reporter who covers state government and politics for the New Jersey Monitor, with a focus on fiscal issues and voting. He has reported from the capitol since 2018 and joined the Monitor at its launch in 2021. The Rutgers University graduate previously covered state government and politics for the New Jersey Globe. Before then he covered local government in New Brunswick as a freelancer for the Home News Tribune. You can reach him at [email protected] .

New Jersey Monitor is part of States Newsroom , the nation’s largest state-focused nonprofit news organization.

Related News

Jersey City tells state: Pompidou can break even with tax credits, $4 million in donations and some aid

- Updated: May. 09, 2024, 5:06 p.m. |

- Published: May. 09, 2024, 5:01 p.m.

- Joshua Rosario | The Jersey Journal

Jersey City made a case for its grand iconic French museum plan Thursday, telling state officials the Centre Pompidou outpost would cost New Jersey taxpayers $19 million each year — and could even break even.

Jersey City Redevelopment Agency Executive Director Diana Jeffrey sent the New Jersey Economic Development Agency a three-page letter accompanied by a brief five-year operating budget for the Centre Pompidou x Jersey City that is short on revenue and heavy on donations and tax credits.

Picasso, Monet, Basquiat, in Journal Square, coupled with a huge youth education component + space to learn for the community is the intention/design of the Centre Pompidou X Jersey City. I am a firm believer (and the independent economic impact studies support it) - that the… https://t.co/X25Rndq03q pic.twitter.com/qwI7pEaNiG — Steven Fulop (@StevenFulop) May 9, 2024

If you purchase a product or register for an account through a link on our site, we may receive compensation. By using this site, you consent to our User Agreement and agree that your clicks, interactions, and personal information may be collected, recorded, and/or stored by us and social media and other third-party partners in accordance with our Privacy Policy.

- IRS Tax Forms

- Connecticut

- District Of Columbia

- Massachusetts

- Mississippi

- New Hampshire

- North Carolina

- North Dakota

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- West Virginia

- Report Outdated Form

- TaxFormFinder.org

- Report Broken Form

- Federal Tax Forms

- New Jersey Income Tax Forms

- New Jersey Form 306 (R-16)

New Jersey Research and Development Tax Credit and Instructions

- Form Content

- 2023 Form 306 (R-16) 2022 Form 306 (R-16) 2021 Form 306 (R-16) 2020 Form 306 (R-16) 2019 Form 306 (R-16) 2018 Form 306 (R-16) 2017 Form 306 (R-16) 2016 Form 306 (R-16) 2015 Form 306 (R-16) 2014 Form 306 (R-16) 2013 Form 306 (R-16)

- Report Error

It appears you don't have a PDF plugin for this browser. Please use the link below to download 2023-new-jersey-form-306-r-16.pdf , and you can print it directly from your computer.

Research and Development Tax Credit and Instructions Form 306 Research and Development Tax Credit

More about the new jersey form 306 (r-16) corporate income tax tax credit ty 2023.

We last updated the Research and Development Tax Credit and Instructions in January 2024, so this is the latest version of Form 306 (R-16) , fully updated for tax year 2023. You can download or print current or past-year PDFs of Form 306 (R-16) directly from TaxFormFinder. You can print other New Jersey tax forms here .

Other New Jersey Corporate Income Tax Forms:

TaxFormFinder has an additional 95 New Jersey income tax forms that you may need, plus all federal income tax forms .

Form Sources:

New Jersey usually releases forms for the current tax year between January and April. We last updated New Jersey Form 306 (R-16) from the Division of Revenue in January 2024.

Show Sources >

Form 306 (R-16) is a New Jersey Corporate Income Tax form. States often have dozens of even hundreds of various tax credits, which, unlike deductions, provide a dollar-for-dollar reduction of tax liability. Some common tax credits apply to many taxpayers, while others only apply to extremely specific situations. In most cases, you will have to provide evidence to show that you are eligible for the tax credit, and calculate the amount of the credit to which you are entitled.

About the Corporate Income Tax

The IRS and most states require corporations to file an income tax return, with the exact filing requirements depending on the type of company. Sole proprietorships or disregarded entities like LLCs are filed on Schedule C (or the state equivalent) of the owner's personal income tax return, flow-through entities like S Corporations or Partnerships are generally required to file an informational return equivilent to the IRS Form 1120S or Form 1065 , and full corporations must file the equivalent of federal Form 1120 (and, unlike flow-through corporations, are often subject to a corporate tax liability). Additional forms are available for a wide variety of specific entities and transactions including fiduciaries, nonprofits, and companies involved in other specific types of business.

Historical Past-Year Versions of New Jersey Form 306 (R-16)

We have a total of eleven past-year versions of Form 306 (R-16) in the TaxFormFinder archives, including for the previous tax year. Download past year versions of this tax form as PDFs here:

Form 306 Research and Development Tax Credit

2021 Research and Development Tax Credit Form 306

Form 306 - Research and Development Tax Credit and Instructions

306 (2012) (09-12) (R-13) - before January 1, 2012.qxp

TaxFormFinder Disclaimer:

While we do our best to keep our list of New Jersey Income Tax Forms up to date and complete, we cannot be held liable for errors or omissions. Is the form on this page out-of-date or not working? Please let us know and we will fix it ASAP.

TaxFormFinder.org Feedback

Help us keep TaxFormFinder up-to-date! Is one of our forms outdated or broken? Let us know in a single click, and we'll fix it as soon as possible.

Virginia R&D Tax Credit Changes: What You Need To Know

Virginia has long-standing research and development (R&D) tax credits in place aimed at incentivizing innovation within the state. The credits are provided to businesses and individuals engaged in qualified research activities in the state, encouraging investments in Virigina research and development.

A recent statutory change alters both how some of the credits are calculated and how they are funded. These changes will affect everyone conducting R&D in Virginia, some positively and others negatively. The new funding change also expands the tax planning opportunities around the credit, so it is important for taxpayers to understand how they will be impacted.

Changes to Both Virginia R&D Credit Regimes

Virginia offers two different credits for taxpayers conducting R&D in the state: the Research and Development Expenses Tax Credit (RDC), which is refundable, and the Major Research and Development Expenses Tax Credit (MRD), which is not. Taxpayers must submit an application each year to the state, which compiles all the applications and allocates set pools of money to all qualified applicants.

IMAGES

VIDEO

COMMENTS

The New Jersey Research and Development Tax Credit TB-114 - Issued December 22, 2023 Tax: Corporation Business Tax ... For more information on the New Jersey R&D credit for tax years beginning before January 1, 2018, see N.J.A.C. 18:7-3.23. If a taxpayer is filing an amended return to claim the New Jersey R&D credit, they must use Form 306 for ...

Beginning with the 2018 tax years, the New Jersey Research and Development tax credit (R&D Credit) will better conform to the federal R&D Credit. Enacted as a supporting bill to the fiscal year 2019 budget bill, Assembly Bill 4202 amends the state R&D Credit to incorporate the current version of the Internal Revenue Code (IRC).

The new credit method is calculated similarly to the federal ASC method where the base amount is 50% of the average of the prior three-year qualified research expense (QRE). However, there are differences: Where there are no QREs in the prior three tax years, taxpayers still apply the current year QREs against the credit rate of 10%.

Credit Law Changes . Tax Bulletin No. TB-114: The New Jersey Research and Development Tax Credit, N.J. Div. of Tax. (12/22/23). A newly posted New Jersey Division of Taxation (Division) bulletin explains certain aspects of research performed in New Jersey and related issues for both New Jersey corporation business tax (CBT) and gross (individual)

New Jersey Research and Development Expenditures - Changes in Deduction Timing: The amended N.J. Rev. Stat. § 54:10A-4(k)(11) introduces a significant change for businesses claiming the Corporation Business Tax Research and Development Tax Credit for New Jersey qualified research expenditures. Starting from January 1, 2022, eligible ...

How to Calculate New Jersey R&D Tax Credit. Take ten percent of the surplus of QREs for the taxable year above the base amount, then add ten percent of basic research costs for the taxable period. Moreover, New Jersey started allowing the ASC method to compute credits on January 1, 2018, but there won't be Code 280C compliance.

New Jersey: New Bulletin Addresses Conformity with IRC §174 and Recent R&D Credit Law Changes. Tax Bulletin No. TB-114: The New Jersey Research and Development Tax Credit, N.J. Div. of Tax. (12/22/23).

The New Jersey R&D tax credit is equal to 10% of the excess of the qualified research expenses for the tax period over the base amount, plus 10% of basic research payments for the tax period, as determined under IRC Sec. 41. The R&D Tax Credit is only available to corporations (both C and S corporations). A New Jersey S corporation's credits ...

R&D Tax Credits. Small business survival and growth requires adequate working capital. One overlooked source of cash for New Jersey manufacturers is the Research and Development (R&D) tax credit. This incentive helps companies to grow by reducing its tax liability for qualified R&D expenditures. Most manufacturers are unaware that their efforts ...

Taxpayers that amortized their New Jersey qualified research expenditures on the 2022 Corporation Business Tax return can file an amended return. N.J.S.A. 54:10A-4(k)(11), which requires an addback of certain qualified research expenditures, only applies to New Jersey qualified research expenditures .

New Jersey Society of Certified Public Accountants, 105 Eisenhower Parkway, Suite 300, Roseland, NJ 07068, 973-226-4494

An R&D tax credit against the entire net income component of the corporation business tax is allowed for qualifying research activities performed in New Jersey. Federal R&D Tax Credit Program Highlights. Every year, more than $7.5 billion in federal R&D credits are given out to companies across the United States. The Research and Development ...

The New Jersey R&D credit provides a credit roughly equal to 10% of the excess of qualified research expenses over the base amount. New Jersey mirrors the federal definition of QREs, as defined by IRC § 41 (b). For tax years ending on or after July 31, 2019, taxpayers should use the Federal rules for computing the New Jersey R&D Credit that ...

The Research and Development Tax Credit (R&D) is a tax credit designed for businesses, regardless of their size, engaged in research and development activities in the United States. This tax credit has a broad application, encompassing a wide range of businesses and industries, extending far beyond the realm of scientists and research laboratories.

The Research and Development (R&D) tax credit is a Federal tax incentive that rewards taxpayers for increasing investment in U.S.-based research activities. ... Thus, a taxpayer with $1M of qualified wages could receive a $65,000 benefit. Many states, including New Jersey, also offer R&D tax credit that can greatly enhance the value of the ...

The Research and Development Tax Credit is often overlooked, but it can provide enormous benefits to companies that recognize its potential. ... New Jersey Cool Program Offers Financial Support for Eco-Friendly Retrofits in Commercial Buildings. Read More. Press Release. November 16, 2023.

(e) The amount of credit awarded to a taxpayer may be applied against the tax liability otherwise due pursuant to section 5 of P.L. 1945, c. 162 (N.J.S.A. 54:10A-5) or the New Jersey Gross Income Tax Act, N.J.S.A. 54A:1-1 et seq., as relevant to tax liability of the taxpayer.

(d) The credit for a corporation that has made a valid election as a New Jersey S corporation pursuant to section 3 of P.L. 1993, c. 173 (N.J.S.A. 54:10A-5.22) may be applied by the shareholders of the S corporation against the tax liability otherwise due under the New Jersey Gross Income Tax Act, N.J.S.A. 54A:1-1 et seq., provided that the ...

Netflix Inc., on track to purchase almost 300 acres of the former Fort Monmouth U.S. Army base for a major production studio in Monmouth County, was designated a "Studio Partner" by the New Jersey Economic Development Authority (NJEDA) last week, giving the entertainment giant access to expanded benefits under the state's Film and Digital Media Tax Credit program.

Capital projects of at least $5 million are eligible for tax credits of up to $75 million in order to elevate arts and culture across the state of New Jersey, increasing the number of first-rate art and cultural experiences for residents and visitors. The broad guideline and legislative requirements for this program have been established ...

The bill, which the Senate Economic Growth Committee approved in a unanimous vote Thursday, would be the latest update to the voluminous Aspire tax incentive program signed into law in 2021, one meant to encourage development, including in some of the state's most beleaguered cities. "We all know of successes the Aspire program has realized ...

Jersey City made a case for its grand iconic French museum plan Thursday, telling state officials the Centre Pompidou outpost would cost New Jersey taxpayers $19 million each year — and could ...

•• For tax years ending on and after July 31, 2023, a registered cannabis licensee that claims a qualified research expense as a deduction on their New Jersey Corporation Business Tax return may also claim that expense for purpose of the New Jersey Research and Development Tax Credit on Form 306, even though such expenses were disallowed ...

The Project Overview. The 1888 Studios project, designed by Gensler, marks the inception of the first campus-style film and studio facility in the Northeast region. Spanning 1.5 million square feet across 58 acres of land, with an additional 20 acres in Newark Bay, the project is estimated to cost $1 billion and is slated for completion in 2026 ...

The letter of compliance will indicate whether the developer or the tax credit holder may take all or a portion of the credits allocable to the tax privilege period. (k) The tax credit certificate shall set forth the following terms: 1. The starting date of the tax period and the commitment duration; 2. The amount of the tax credits; 3.

This paper uses detailed study of a proposed research and development (R&D) tax credit in one U.S. state, New Hampshire, to gain insight on an important public finance issue: the motivations for and the economic costs and benefits of R&D tax credits. the paper reviews the policy considerations and assesses the potential economic impacts of enacting a proposed R&D tax credit in New Hampshire in ...

Overview Virginia has long-standing research and development (R&D) tax credits in place aimed at incentivizing innovation within the state. The credits are provided to businesses and individuals engaged in qualified research activities in the state, encouraging investments in Virigina research and development.